A lock extension is what is required when a loan does not close in the time frame as arranged with the original lock. Locks are available for 30, 45 or 60 days with the longer the period of time available for the lock, the higher the cost. So if you have a 30 day lock and for what ever reason, your transaction has not closed by day 30, you’re in a situation where the lock may need to be extended. It used to not be a huge expense if you were 1 day late past the extension, most lenders charged around 0.125% for an additional 7 days (extensions are typically offered in blocks of time, like locks).

Our government elected to pay for the Temporary Payroll Tax Cut by demanding a 0.10% fee on all new mortgages generated by Fannie or Freddie (conventional) and FHA. This roughly pencils out to an increase in rates of about 0.125% give or take. What some banks have also done, is to increase the cost to extend loans. Some banks/lenders are calling this “temporary” and others are not.

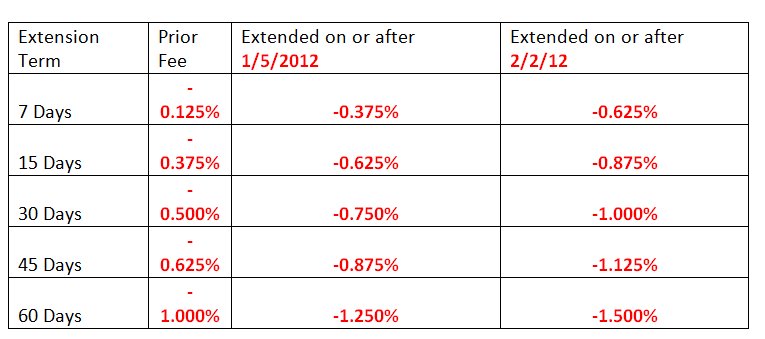

Here’s a sample from one lender who recently increased their extension fees for a second time!

For example, if you have a $300,000 loan amount, prior to the government’s “G-Fee” your extension fee would have been 0.125% of $300,000 = $375. After February 2, 12, with this lender your cost to extend a rate for 7 days is now a whopping $1,875.

Every lender has their own extension fees. I recommend asking your originator what the cost may be should you need to extend.

Other possible options to consider, depending on where rates are should your lock be expiring, is letting a rate expire and re-locking, if your lender permits. Lenders have different policies with that as well and it’s important that you discuss this with your mortgage originator.

How did I miss all of this? I am going to contact my mortgage guy here in Virginia to get up to speed!

It seems to me that that extra little fee (your other post) will not help stabilize the shaky home buyer market across the U.S. of A. What were they thinking?

Doug, it’s forcing consumers to lock a little longer, which also is a bonus for the big banks 🙁

I won’t expose the Too Big Too Fail bank who is cramming those fees down on consumers.

Of course, the problem is there are still a lot of boiler rooms/shady outfits that are quoting 30 day rate locks to make their rates look lower than the competition knowing damn well the odds of getting a refi done in 30 days are next to impossible on even the most perfect file – HVCC, over zealous underwriting, three day recission periods, etc.

Given the cost to extend under the new terms, that .125 difference in rate really is more expensive than getting an accurate rate quote to begin with assuming longer lock periods.

We can also thank the new LO comp laws too… No longer does the LO bear the burden of extensions.

I think it’s the clients choice for how long they want to lock, however they need to know what the cost to extend may be. Nobody *plans* on extending…but “extensions happen”… and now that a majority of the lenders have jacked the cost, it’s probably better to err on a longer lock period than risk an extension fee.

It is their choice, but that assumes they are truly informed of the risk. My experience has been that 99% of borrowers have no idea about rate locks. Further, the borrower isn’t going to know what is appropriate in terms of time frame needed to actually close.

it is their choice AND it’s a mortgage originators responsibility IMO to make sure the borrower understands how their rate lock commitment works and what the risk are.

Thanks for sharing this Rhonda! Since this is a choice, it is totally important that the buyer plans and studies every factor that is related with it. Yes, you are right, extension is always the least that any buyer would like to encounter. But most of the time, “situations” crop up putting them in a point when they have can do nothing but bear with.

Congratulations to this very interesting and timely post!

Thanks for the useful information, I agree that most of the borrowers does not have any idea about this, I hope that mortgage originators explain everything to them.

Oh no, another expense for home buyers. and the sadder part is that most of these buyers are not even familiar with this rate locks.

This is just absurd. Doesn’t anybody see that the regulation is the culprit? Regulators want a cut, so the banks passes the cost to the consumers. The consumers think is the bank’s fault so they protest against the bank and tell the regulators to do more. It’s a vicious cycle.

Happy to report that one of the big banks we work with is reducing their extension fees – not back to the previous levels (about 0.125% higher than what used to be the “norm”) — still a much welcomed improvement to the recent adjustments. Now lets hope the other big banks follow and reduce their extension fees too!

This is long done. FHA getting more expensive in April too

To those reading this blog, kudos. Rhonda is a legend, don’t pass up the opportunity to work with her

Thanks, Jonathan – you’re going to make me blush 🙂

I try to let folks know that even if rates stay low or go lower, the COST is getting more expensive.

Our mortgage co never told us about the extension fee. We started the process in october and never heard back from them again till January and they informed me that we had two lock extensions. One was because my company never called them back to say i worked there. I feel they should of called me and I would of gotten my company to call asap. 2nd was there fault and they never told me about it till it was two days before the closing!! They sent me two huds and both where totally different then the other. They now want me to bring $1700 to the closing which I was informed 1 day before the closing. I think we are going to back out. Bad communication from the mortgage company. Opinions?

Hi Mindy, have you discussed this with your mortgage originator?

Due to the Fed’s “LO Comp” regulations, your mortgage originator cannot absorb any cost associated with your mortgage. However, their mortgage company might be able to chip in for some of the cost. When I have an extension situation, I review the file and determine if the borrower provided everything to me promptly or if they (or their employer) were contributed to the delays… did the borrower take a vacation or did things that happen that were unforeseeable. Ideally the mortgage originator or their processor probably should have contacted you when your employer did not respond quickly. If I feel the blame for not closing before the lock expired is 50/50, I’ll see if management can help with the cost by splitting it with the borrower.

Before walking away from your refi, know that rates have been trending higher – if you want to refi, you may want to price out what your scenario would look like if you were to start over today. Also factor your appraisal fee (if you had an appraisal) as most lenders will not accept appraisals from other mortgage companies (you can thank your elected officials for HVCC and AIR).

Good luck!

No one was on vacation. I just feel it was poor communication on there part. If i knew there was a chance that I would have to bring $1700 cash to the closing I would not of started the process. First they told me I needed to bring $30 to the closing then $118 then 1 day before $1700. They told me they would take some money off for the extension due to their fault but they won’t take the extension off for my works mistake. So now i have to bring $1200 to the closing which is still pretty high for me. On the hud they have the $1700 included in the closing costs and then they tell me I need to bring $1700 to the closing. So that does not make sense to me. I asked him about that and he said he would talk to his boss and then called but never told me why it was also on the hud. We would save $200 a month but it will take me 4 years to make up the $1200 and the closing costs. Mindy

Hi Mindy, do you know how long the lock period was for? Was it a 30 day or 60 day lock? Did you select this lender because they had the lowest rate/fees or were they referred to you?

Hi Rhonda, i went with them because it was the mortgage co I have now. I didn’t have to send them any paperwork or they didnt have to do an appraisal on my house.

I’m sorry Mindy. Extensions are not uncommon in this market because of how busy lenders are. However they do need to be disclosed. You have a three day right of rescission that takes place after funding – three postal days must pass after signing before your loan can fund. This is to give borrowers time to decide if they still want to proceed with the closing.

Sometimes extensions are not disclosed until the end because that’s when the lock expired.

Do you know when your actual lock expired? Did the LO contact you then? If they just waited until escrow to disclose the fees… that stinks.

Mindy, what % is the extension fee? For example, some of the lenders I work with charge 0.25% to extend a lock for 15 days.