Can Seattle Home Prices Drop Another 22% was a question raised by many here in the Seattle Area, after Zero Hedge posted the Goldman Sachs forecast for Major Cities showing Seattle at a 22% drop by year end 2012. After calling for modest to almost no declines in several major cities, Goldman predicted a 22% drop for Seattle with the 2nd highest drop being only 12% in Portland, and even a 7% gain for Cleveland Ohio and a 5% gain for San Diego. That would put Seattle at minus 27% compared to San Diego for the same period.

You can pick up Goldman’s rationale or lack thereof in that first link, we’ll stick to how likely it is that Seattle could drop “another” 22%. First let’s take a look at where a drop of that size would takes us, in the graph below.

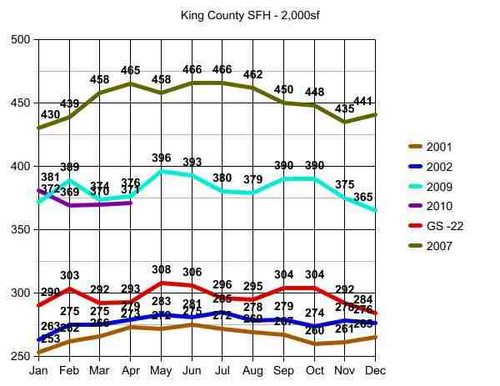

Important to note that I made a slight modification of the raw data for the graph above to account for modest home size variances, equalizing the data as to size of home or price per square foot. The closest rounding point was a median sized home of 2,000 sf. The data is in thousands, so top left in January of 2007 would be $430,000 median home price for a 2,000 sf home and bottom left would be $253,000 for a 2,000 sf home in January of 2001.

I posted a full chart of all of the raw data for those who want to create their own charts and modifications showing actual median home prices for the years in the graph above, median square footage of homes sold in each 30 day period and the # of homes sold. This is for Single Family Homes vs. Condos and King County vs. Seattle Proper.

Back to the graph above in this post. The top line is Seattle Area Peak in 2007. The turquoise and purple lines are “where we are” in 2009 and 2010 without significant difference except for seasonal variances in that 18 month period. I ended these graphs and the data at April 30 2010 due to the switch out of mls systems locally, but am seeing reports that May came in above April at $379,000. So the raw data suggests there is the normal seasonal bump up in May, as additionally influenced by the final tax credit closings which will continue until after June closings, and possibly slightly beyond.

The red line is the hypothetical Goldman Sachs prediction scaled against 2009 data at 22% below in each consecutive month.

********

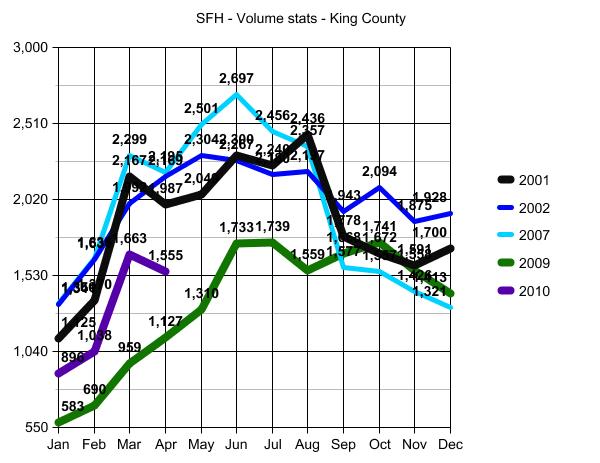

Before moving to conclusions, we need to visit the volume stats (graph below). I have been tracking volume for years in addition to price per square foot, as volume signals recovery or not more so than home prices alone.

Analysis is dependent on rationale of which data to apply, and for my purposes I have been using 2001 and 2002 as “Base Points” for two reasons:

1) 2001 is the earliest I will go when tracking home price and volume data, as Credit Scoring as the primary focus of lending pre-approval guidelines and risk-based pricing, was not a factor in the 90’s. Keeping apples to apples as to the number of people who can qualify to purchase a home, 2001 is a good start point.

2) 2003…toward the end of 2003…was the beginning of ZERO down/sub-prime lending standards. So all years from 2003 through mid 2007 will include an extra bump up as to volume and price created by that loosest of lending standards.

For both of the reasons noted above, it has been my long standing premise that volume of homes sold should be and can be expected to return to 2001 and 2002 levels as to number of homes sold.

One caveat: The number of condos built between 2001 and present is beyond proportional. Those additional “residences” in the form of condos and lofts in the Seattle Area will rob volume from the single family stats in some, and many, areas.

Note: In the second graph above, the volume of homes sold in October of 2009 (green line) exceeded the number of homes sold in October of 2001 (black line). This may not seem like something to view as a positive sign. But given the tremendous drop in volume as noted in January and February of 2009 to unprecedentedly low levels, surpassing 2001 volume stats by October of that same year was HUGE. Of course these numbers at both ends are influenced by the short breaks in the tax credit for home buyers in both January of 2009 and October of 2009…but still a significant signal reflecting that volume has the opportunity to recover to 2001 levels. NOT to 2007 levels! Volume cannot and will not recover to 2007, nor do I expect prices to do so until 2018 at the earliest.

Those who are waiting for a return to 2007 as to price and/or volume would likely have better luck betting on your favorite horse.

********

So, just how low will Seattle Area Home Prices go? Well first off let’s acknowledge that Seattle Area Home Prices WILL go DOWN. That seems obvious to me from the RAW DATA, but amazingly I still see many people questioning whether or not the market will go down at all from here. Hard to believe, but yes, some think the current level of $379,000 median home price is going to go up and not “EVER” down from there. One would think the credo of “home prices will never go down” was dismissed along with The Easter Bunny…but no. Some are still looking for a V-Shaped or U-Shaped “Recovery”. Sad but true.

A- Home prices will most assuredly drop by 4.3% in the very near future and likely by 4th Quarter 2010. (See blue square in the RAW DATA link above.) That is where home prices were in March of 2009 before the tax credit was renewed. So seems obvious without the credit, that is where prices will go back to…and likely lower than that without a new tax credit to prop up prices from that point forward.

B- The Tax Credit was meant to stop the downward spiral and eradicate the portion of loss created by momentum and NOT the portion of downward spiral created by fundamental economic problems. It was to eliminate the Fear Factor and the over-correction. Not the market’s legitimate decline point. Consequently the “safety net” being removed is going to create an additional drop of at least 5% in addition to the 4.3% drop noted above, which would take us to a drop of 9.3%.

C- Goldman Sachs is incorrect in its analysis of a 22% drop, because they do not apply the above A and B factors to all Major Cities. So their basic rationale is not credible, nor the number that emanated from that incorrect rationale.

D- Near the end of the time frame for the tax credit, home buyers were not as likely to enter into contracts with short sales and to some extent even bank-owned properties, for fear they would not close on time. Consequently, the median home prices were overly weighted to the high end of my bottom call. The mix of property from here through year end is going to push more toward the 37% under peak of that same bottom call vs the 20% side of the equation, with more “distressed” property in the mix. Not because of increased foreclosures, but because of more people being willing to buy them without a drop-dead-must-close date via the tax credit. It’s really just common sense, and pretty much a given.

Look for a 9.3% drop at some given point between now and the end of 2011. That would be any month in that period with a median home price of $343,753 or thereabouts.

As to 2012??? I expect a significant impact on price, with further declines, stemming from continued layoffs between now and the end of 2012 on a fairly large scale. But this last prediction borders on “the crystal ball method”. So let’s end with a 9.3% drop from $379,000 median King County home price by year end 2011, with an added caution that significant improvement to 2007 price levels will not likely happen before 2018.

In other words…”EXPECT the worst; HOPE for better than that.”

(required disclosure – Market Observations and all stats in this post and the graphs herein are the opinion and “work” of ARDELL DellaLoggia and not Compiled, Verified or Posted by The Northwest Multiple Listing Service.

Hey Ardell, quit trying to suck the sunshine out of the day 🙂

A few positive rays: Stable employment with the “higher paying” industries will be key for the upper-end housing market. New stimulus needs to come in the form of middle class job creation rather than temporary home buyer credits to keep the affordable end clicking along…long term.

The dark horse I’m betting (more like hoping) to short is inflation. Continuation of low interest rates gives us a decent chance to keep some stability at present pricing levels.

Admittedly pulling for several “ifs” but agree with you the the -22% scenario is highly unlikely!

Rob

Rob,

When you get the weather man to tell you it’s going to be sunny in Seattle EVERY night on the nightly news before you go to bed…come back and I’ll become a real estate cheerleader for you. 🙂

22% seems pretty tame to me.

I looked at average wages for Seattle and was surprise at how many $100K a year slots there were for soft ware engineers. There are also the attorneys that go along with that.

That was Census Data, which will be completely updated in the next couple of months. Now when you couple that with the amount, the sheer volume, of housing units created in the down town core alone, you know sales price data will slip by at least 22%.

Seattle is unique in that it lost momentum last. We are still building, with Paul Allen, Microsoft dollars at South Lake Union. Only gawd knows what has happened on the Eastside, because that is another area that went through massive development.

Cleveland, and San Diego, took hits immediately, and in my opinion, more deeply than Seattle.

Ouch. I simply cannot see a scenario in which the home prices in Seattle drop another 22%. Yes, Seattle begin to decline in price after many of the cities in the United States, but no, it will not continue a linear decline very far past these cities. This is in part due to the lower than expected lending rate (thank you Greece),replacement cost and the lack of new construction.

Grant,

Let’s examine that, because no one should ever deny the possibility of a potential 22% loss when they in point of fact just experienced…by all accounts…a 22% loss in pretty much a one year period, that period being 2008 in the Seattle Area.

The down/correction phase is supposed to be 3 years in housing, not one year. If not for the tax credit we ALL agree the market would have continued to decline in 2009 and early 2010. EVERYONE in the freakin’ World agrees that the tax credit propped up home prices. I don’t know anyone who disputes that fact.

So to deny that the tax credit going away will have an impact on home prices borders on ludicrous.

Now let’s look at The Dow. The highest closing of The Dow was at 14,164 on October 9, 2007. That number is much like the graphs in my post with the highest median price being $466,000 in the summer of 2007. Today The Dow is at 10,300, that is a 27% drop. I think The Dow could feasibly be at a 44% drop from its peak of 14,164, which would be 7,930. In fact it went well below that, and was in recent history well below it’s current level of 10,300.

If the stock market can go down 44%…so can the housing market. What is possible in one market, is likewise possible in another.

So if you say to me that the Dow can’t go down by more than 10% (9,270) and the housing market cannot go down more than 10% either…well, OK. You’re entitled to your opinion.

BUT if you say The Dow could get to 8,000 but the housing market can’t go down another 22%, which would be the equivalent scenario, then what you are really saying is you simply refuse to and do not want to believe that, and that is your right.

Personally I think the stock market can get to 9,000 in a heartbeat and likewise the housing market can also get to the equivalent drop of 12.6% in a similar heartbeat. Knowing that The Dow was down to 6,500 not all that very long ago…tells me most anything is “possible”.

What has happened in the recent past…can very easily happen again. The handwriting was already on the wall…so those who refuse to recognize the possibilities after having seen that handwriting on the wall…are simply refusing to “see”.

I cannot say it is absolutely going to go down 22% anymore than you can say it is absolutely not going to do so. The minute someone grinds in their heels and says “not possible”…that is simply an emotional stance, and not an informed position based on all data available.

That you “simply cannot see” it is like saying you are closing your eyes because you simply do not want to…because lots of things are “possible” and recent history has told us so.

David,

I haven’t peeked into the Pandora’s box of condo stats in ages. You mentioned Downtown and a few other things that group condos with single family homes. Note that the stats here do not include condos. Without condos in the mix, are your feelings the same as noted above?

I’m putting a condo in the mls shortly in The Newmark by Pike Place Market, I may have a better feel for what’s happening Downtown in the next couple of weeks as a result.

http://www.realtown.com/Ardell/blog/condo-seattle-view-downtown-newmark

The condo stats aren’t the issue. It’s the development. The continued building, the growth, the money, that’s what is missing today. Now, in a hind sight, any one can see that there was a bubble, prices were high, and the new normal will be a lower price per housing unit. Seattle was still developing when the rest of the country was in crisis.

You couple that with my first statement about wages http://www.payscale.com/research/US/City=Seattle/Salary and you can see Seattle was a sweet spot for investment.

There are two questions, the first is about the wages, and those projections, the second is if Seattle, the Estaside, King County, are over built.

My impression is that the bio tech industry that Paul Allen was targeting won’t materialize here in Seattle. Second is that software engineering, and tech support wages will erode. Seattle, for all the integration of tech industry jobs, is still very blue collar. We are missing timber, and fish, but we still have shipping, and ware housing. Wages could be a topic of discussion.

More to the point is all of the high priced property that has sold in the past three years since 2007. If we just look at the 23% decline Case Schiller says we have had, and if we rely on sales data, then we for sure have a ways to drop.

You have to go back to 1998 to really see Seattle Real Estate pricing. Before Windows 95 Seattle was that other Washington. We were a back water of fisher people, and loggers. In a burst of buying frenzy we had Phinney Ridge houses selling for a half of a million dollars. We had bidding wars from cash buyers. It got out of hand quickly. Then after the lawsuit in 2000, when all looked lost, the frenzy started all over again.

Anyway, a 45% drop from the peak seems fair. We had a long peak.

I don’t disagree with that, David. I think it’s a valid perspective. Thanks for sharing.

As an absolute aside, I was looking up a property that will be coming on the market in a few weeks. It was bought in 1996 for $139K, and resold in 2002 for $262K. I’m not sure other parts of the country saw that kind of appreciation, at that time. 88% per cent appreciation in six years.

I do think many other parts of the Country did see that kind of appreciation, David. 1998 to 2005 in most areas of the Country had a higher degree of appreciation than the Pacific Northwest.

A condo townhome (no land value involved) I bought for $545,000 in 2001 and resold for $685,000 in 2002 and the person I sold it to resold it for $1.350,000 in 2007 or so. The current owner has been trying to sell it ever since he bought it with no success. His last try, likely a short sale, was down at $838,000 when it was taken off the market or maybe when into foreclosure on June 3rd of this year. That was in Manhattan Beach CA.

So that would be appreciation of 147% from 2001 to 2007ish and a drop of 38% at least. Can’t pinpoint it exactly until someone actually buys it.

The REAL story of the market is in properties like that one that are not selling at all. The market is not about what SOLD and what price it sold for…the market is much more about all the properties that no one wants to buy, period! I think we will see more of that without the tax credit.

David…just checked another that I sold in 1996 for about $195,000 (similar to your example) back in PA that is now valued at $463,000 after the price dip.

Yes, David. Many areas had not only similar appreciation…but even more. Pacific Northwest in many if not most areas did not enjoy the high levels of appreciation much of the Country saw between 1998 and 2005. A lot of our appreciation came in 2003 to 2007 with loose lending being the pusher. That is the portion that we have lost to date.

I don’t think we are a “lagging” market. I think what will hit us will hit all markets, similar to the sub-prime crisis. That is why even if Seattle did see drops beyond what I have predicted to what Goldman Sachs is saying, Goldman still has to be dead wrong. Because that will not happen in the Seattle Area while the rest of the Country is not similarly affected.

But, as an aside, I feel a nasty amount of layoffs coming in the next two years…hope I’m wrong on that. We are not as well diversified as a work force as you suggest we are. One big company with massive layoffs will not be something this area can work through…

This site is extremely frustrating. It’s very difficult to submit a comment, but let’s try this again.

Real Estate appreciates at about 4% per year. The price of housing units is tied to, but not a part of the Consumer Price index. Inflation is easier to show

http://www.inflationdata.com/inflation/images/charts/Annual_Inflation/annual_inflation_chart.htm

With inflation at about 6% at it’s peak, you can see that the price of housing got way out of control. A 45% drop from the peak seems extremely reasonable. Like I said you have to go back to 1998 to actually see that the rate of appreciation was pure fantasy.

My point about Seattle lagging was the amount of development that was still going on here after other markets had already crashed.

David L,

I don’t go back to 1998 to see the rate of appreciation (not saying you shouldn’t, of course) because here’s what I saw in 2005.

Take a townhome complex. (I have a specific one in mind where these were accurate numbers for what was happening in 2005). EVERY sold townhome was selling for 5% more than the previous one. Appraisers were allowing a 5% increase. perhaps meant to be for the year. BUT every appraiser was applying the same 5% above the last one and every seller was asking 5% above the last one and every buyer was paying 5% above the last one.

It didn’t matter if “the last one” was a year ago or a week ago. As soon as other owners saw the prices going up, many started putting theirs up for sale.

So I saw a 35% increase in home prices in that little community in a 4 month period!

5% up per house was a good norm in 2005. So if two houses sold, then the neighborhood went up 10%. If SEVEN houses sold (5% up per house times 7 houses) then the neighborhood went up 35% during the Spring Bump period from March through August.

Taking that 4 month 35% increase and annualizing the rate of return back to 1998 to call it only “6% per year”, when it was 35% in four months, makes no sense to me.

That 35% was a bubble of air…created by unrealistic factors, in a four month period. 6% a year vs 4% a year is not a “bubble”. 35% in 4 months is a “bubble”.

As to your comments on development…I really never understood why a market was supposed to support continuous new construction. Makes no sense to me since I have for 20 years pretty much worked in 100% “built out” communities with no available land. I don’t support the concept of new houses being built all the time, as that puts undue pressure on resale homes. I am primarily and almost exclusively in the business of resale homes. So for the most part I don’t like to see new construction, except for the teardown of an eyesore or major deferred maintenance dwelling that is hurting the property values of the neighborhood.

Not to argue your point…just my $.02

Further to David L. I do see two of your comments in the spam bin along with 110 real spam comments. I didn’t release them as all 3 are about the same and would duplicate the message. From what I can tell it is not only that you put a link in the comment (which invites the great spam gods of the internet to whack you) but the source of the link. Some links make it through and some don’t.

I suggest for awhile you try posting your comment without the link and then posting the link in a separate comment, just so we can see if your comment goes to the site but your link comment goes to spam.

Sorry for your frustration. I expect we have our spam filters set on a high filter level so we are not spending our time deleting those other 110 spam comments. From what I can tell some of your links are to more reputable sites than others, and so some trigger the spam filter and some do not.

Ardell, I just love the numbers and stats and the way you work through them and present them. Beautiful. Thank you.

I think you just sent a cold shiver through the spine of any current or potential seller that might have read this blog though.

This might tend to make a potential buyer such as myself feel good about the situation, it does not. As you state,

“The REAL story of the market is in properties like that one that are not selling at all. The market is not about what SOLD and what price it sold for…the market is much more about all the properties that no one wants to buy, period! I think we will see more of that without the tax credit.”

You are spot on. This is precisely the problem we are running into. Lot’s of properties we are looking at are priced above the median Seattle area price that we just do not want to buy. They lack quality and value.

It is a terrible vicious cycle we are now in. The more values go down, the less inclined the buyers, the more likely listings will stagnate on the market.

Still looking,,,

I am in the same boat. This blog post scares the crap out of me!

We just received mutual acceptance on a house in Ravenna.

Bottom line for us is that we found a home that has everything we want and one we can grown into over the next serveral years. There are a lot of houses at the 500K mark that don’t meet the level of quality and value so we upgraded a bit to the 550 range and our options increased quite a bit.

I anticpate another 5-10% decline over the next couple years.

cj

You said: “I anticipate another 5-10% decline over the next couple years.”

Let’s call that a given over 18 months since my 9.3% and your 5% to 10% are not out of line with one another.

The reality is this:

If you just paid 6% more than most people would pay for that house today (current market value), then you have already used up a large portion of your future decline allowance. If “the market” goes down 9% your house goes down 15%, because you have to add that 6% overpaid to the 9% decline generally.

If you just paid 6% less than most buyer’s would pay for that house today, “the market” can go down 6% before you “lose” a dime, and so if it goes down 9%…you only lost 3%.

You can and should read about current and projected market conditions, but nothing will replace choosing wisely, and it’s every man for himself when it comes to utilizing the information you gain by reading potential future outcome, and managing your personal risk accordingly.

You also said: “This blog post scares the crap out of me!”

Maybe this will help with that. The NUMBER ONE reason people lose money when they sell a house is because they HAVE TO sell the house at the “wrong” time.

1) Because of Divorce

2) Because they lose their job

3) Because they are just not happy with the house or where they are living and losing money becomes secondary to being absolutely miserable vs. happy/happier

SO to manage your risk against future loss on the “sale” of your home you should do these things.

1) Be very, VERY nice to your wife (or partner who helps pay the mortgage) so that they will not leave and by doing so leave you with the need to sell at a loss.

2) Work really, really hard and don’t be a slacker. If your company lays off 10% of the workforce, you do not want to be the one out of nine who is let go.

3) You are already in escrow, but for those who are out looking for a house, choose the WHERE first and know you will be happy THERE. Do not focus so much on the WHAT, that you end up with the right WHAT in the wrong place. Try to make sure the neighbors are not such that your life will be miserable living next door to or in between them. The rear neighbor as well. Awful neighbors can make life unbearable.

Limiting the reasons why you might have to sell at a loss because of those three things…will give you more protection against $ loss than reading 1,000 blogs forecasting future market conditions.

If you could not keep the house if you got a divorce, as example, do NOT ignore birthdays, anniversaries, etc…and do not put your wife down (or husband) three times a day.

More money is lost due to divorce in a down market than most any other reason, and once you have set the stage for someone to want to leave…it is too late to reverse that damage when you realize it is going to cost you your entire down payment.

Those things are WAY more important, in reality, than knowing where housing prices will be 5 years from now.

Thank you David.

In my opinion THE most important aspect of contracts is “informed consent”. If people are taking a gamble in uncertain times, then we should not lead them to believe it’s “a sure thing”.

In the last 30 days I overheard an agent tell a buyer “yes but if you buy it now for $400,000 in 3 or 4 years it will be worth $500,000” (exact words I heard out of an agent’s mouth recently) and a seller say “I want to hold it for another year or two and sell it when prices are better”

I don’t want to send shivers down anyone’s spine, but when I hear things like that it behooves me to open Pandora’s Box and spill the beans.

As to your situation, remember that my definition of Fair Market Value is the price at which neither party is exceedingly happy.

Every seller who is selling is looking at the top line in the first graph wishing they had that old price from summer 2007. So no matter what they get…full asking price even, they are not “exceedingly happy”. They don’t want to get as close to the turquoise line, current values, that they can get. They want to get as close to 2007 as they can get. You’ve been out there…you know that’s true. 🙂

Every buyer who is buying is looking for a little protection against future declines by buying below today’s values in the turquoise and purple lines.

I am currently helping someone who is refinancing a home they purchased in order to eliminate PMI and get a lower interest rate, both. It’s “Truliaboy”.

http://raincityguide.com/2009/10/07/truliaboy-gets-his-house-and-a-puppy/

He bought the house for $275,000 or so just over six months ago. At the time he bought it, it appraised for $325,000, but at time of purchase PMI (Private Mortgage Insurance) is based on value or purchase price whichever is LESS. At the time of purchase all of the comps used by the appraiser were distressed properties. This time of year going back 6 months, the comps are NOT mostly distressed properties. If he can get an appraisal on a refinance at $350,000, he can reduce his interest rate by about .5% AND get rid of the many years of PMI payments.

If the market goes down “another” 20% from here, the value will still be what he paid 6 months ago. So no, I don’t want to send shivers down anyone’s spine. I want to arm them with the information they need to enter into contracts wisely.

Articles like this help me help my clients. If I don’t dig deep into the stats and formulate a strategy for my clients from my findings, then I am not doing “my job”. To do my job well I have to help my clients manage risk. In order to manage risk, I have to know what that risk is, so we can do our best, the clients and I, to manage that risk. Truliaboy managed risk by achieving a below market price at a time when the market was positioned to go down vs up.

A lot of people ask me why I blog. By laying everything out in front of me, putting all the cards out on the table and getting feedback and input from anyone who grants me the opportunity of picking their brain by stopping by and commenting, I am arming myself with everything I need as a real estate professional to better assist my clients.

That is why I am extremely grateful for your input and why this statement from you means so much to me:

“Ardell, I just love the numbers and stats and the way you work through them and present them. Beautiful. Thank you.”

That this information may help you is a byproduct of blogging. What I’m really doing is checking and double checking my thinking and the information I use in that thinking, so as to better and best assist my clients.

I very much appreciate your taking the time to comment. I wish you luck in your search and articles like this will help you understand why your home search leaves you feeling “They (homes for sale) lack quality and value.” The reality is that for a buyer, the value lies at LESS than today’s prices and for a seller the value lies at MORE than today’s prices.

“Overall Market Conditions” will never satisfy any one individual’s needs. The hard work of home buying and home selling is finding that ONE property or that ONE buyer among many that will suit their needs. The market as a whole can never offer best conditions. It is “your most important asset” and that means…it ain’t easy.

Ardell:

Totally agree with:

“The NUMBER ONE reason people lose money when they sell a house is because they HAVE TO sell the house at the “wrong

Best Case I see as 4.3% to 9.3% down, due to seasonal variances and the tax credit going away.

Worst case could in fact be 22%, but only if the stock market crashes back to 6,500 and/or at least one, that being THE largest one, or more of the five largest local employers cutting staff by 10%.

Massive layoffs of “only” 10% could easily happen and without much advance warning in 2011 or early 2012, and that will signal the bell for below 9.3% as to drop in home prices.

Given the economy, it is not outside the realm of possibility for the two largest employers to drop staff by 10%. I am going into places OFTEN these days and seeing 10 desks with 4 EMPTY. Many companies have more space than they can afford to have people to fill that space.

The handwriting is on the wall…

Thanks much!

So, if this house was remodeled completely and sold Sep. 2004 for $515 and our offer (after several rounds of counters, and after several price drops) settled at $542.5 (not incl. $10K back), which equates to 5.3% total appreciation in almost 6 years.

The house has 2.5 baths and 3 Brs all on the same level, and a refinished basement with a 4th BR, although it wasn’t listed as a 4th bedroom because no closet (thank you for being honest listing agent!).

We expect to raise a family and live there for at least 10 years or so (you are dead on re: #1 and #2 above, by the way!)

I know the market is what it is at any given point, but do you think this sounds like a reasonable deal in today’s environment?

cj,

I’m not really allowed to discuss that when you are in escrow, but email me the address when it closes and I’ll give you my $.02. In fact I’d be happy to drop by and tell you what improvements will pay off and which will not based on the house and its location, so you have a long term improvement plan. I walk Green Lake in good weather (walk at the gym most of the year) and can walk to some parts of Ravenna from there.

Keep your eye on your closing for now… 🙂

Oh, and cj, I don’t understand what RobH’s problem is. If you can shed any light on that for me, I’d appreciate it.

That sounds like like a much more realistic appreciated value, from that previous date and price, than much of what we are seeing in our searches of Maple Valley listings. I’m not a realtor, I’m a prospective buyer too, so that’s what I think. I am frustrated by 30% to 60% appreciation (at least in listing price) from nearly the same date. But I’d imagine the sellers are too, the properties have been listed for months. Many of the listings seem to be nothing more than a ‘we’ll sell if someone will pay us this much for it’ listings.

Well priced houses are still moving albeit slowly, we just need them to have the things we want (ample parking) and location (Maple Valley).

Congrat’s to you cj for at least having a closing date on something.

David,

Historically home prices (asking prices) either go down, or the seller decides to not sell at all and takes it off market, between 9/15 and 11/15 of each year. Some come back three or four months later, as that kicks the cumulative days on market back to zero.

I think you will start seeing some relief in pricing by end of July. One of the problems with lots of really bad weather is sellers do not feel like their price was tested well until a few consecutive weeks of sunshine. People laugh that agents blame poor sales activity on the weather, but the reality is that sellers do that as well.

Thanks, David and Ardell.

It’s far from a done deal however, as new FHA underwtiting requirements are quite strict. Looks like there’s some major repairs (exterior paint, sewer line replacement [sewer scope is a must!], and more) that the seller would have to take care of before funding/settlement. FHA basically inspects/approves the apprsaisal and that level of scruitiny (well any scrutiny) is quite onerous.

It’s in the sellers hands now. If he wants the deal to happen, he has to make the improvements. Three weeks and counting…here’s hoping it all works out.

wow…can’t comment on an escrow in progress…but let’s talk about that more when the dust settles. It will help other home buyers to clarify some of that info. If you are willing, I’d love to interview you as its own post when all is said and done.

Awesome ARDELL, you always seem to have a way to keep yourself in the news and get people to read your blog! 🙂 Good job.

Just like, in 02/2009 you said “I’m calling bottom”

http://raincityguide.com/2009/02/07/were-at-bottom/

And then posted a bunch of analysis in 03/2009 to justify your “bottom call”

http://raincityguide.com/2009/03/30/sunday-night-stats-snapshot-of-bottom/

What about all of the above? Of course, public memory is short so nobody probably remembers your famous “bottom calls”.

Seems like you’re sole purpose is driving traffic to your blog, posting a bunch of sensational stuff and then justifying what you posted in the short-term. After all, Real Estate agents need to make money isn’t it? By saying prices will drop another 23% you want sellers to drop their prices early, get more buyers interested, you get your commission and leave. Hah!

I’m predicting your next post will be in a few months to justify what you just posted around 23% price drop, why it’s happening or not happening. Have fun.

Hi Rob,

People don’t need to “remember” because THAT bottom call is IN THIS post AND I highlighted that exact point in the RAW DATA and outlined it in blue. Just hit the RAW DATA link and you will see it.

That bottom call you refer to is still holding and is part of this post, which you apparently did not read. That bottom was $362,700 and we are at $379,000 and we have not since my call been lower than that call or even near that “bottom” yet.

So if your point was that my bottom call was incorrect and/or did not last from then until now and beyond today…you would be incorrect.

Read this post and hit the links and you will see that “bottom call” and understand that I was indeed correct, and as far as I can tell, the ONLY correct “bottom call” of the many.

Have a great day! If you don’t understand who is calling the 22% drop (it’s Goldman Sachs and a major news story, not “my” call) then you need to read the article and not just “the headline”.

Snarky’s cool…but wrong information is not.

Goldman Sachs stock is more likely to fall 22% b4 years end than Seattle home prices

MeHoff,

I agree BUT no one, not even Goldman Sachs, ever said Seattle home prices would fall 22% by year’s end.

Goldman said 8% by end of 2011 and 22% by end of 2012 and said nothing at all about by the end of 2010.

I said 4.3% by end of 2010, 9.3% (another 5%) by end of 2011 and with the assumption of major layoffs in 2011 and or 2012, then that 9.3% could be double or more (down from here) by end of 2012. The starting point being $379,000 median home price. 4.3% down being $362,700 (same as it was in March of 2009). 9.3% down being $343,700. The numbers are cumulative from here.

We will be lucky if it only declines 22%. There is a laundry list of economic indicators that support this. Not to mention, the money the government was spending to help bolster the economy is going to last forever. Small business which provide over 80% of the countries jobs are not hiring, if anything they are scaling back, hence unemployment will continue to rise. The cost of living continues to increase while employers are putting freezes on salaries. Lending guidelines continue to be very strict, as they should be. I could go on and on, but taking a look at the whole picture the worst is yet to come. Mish’s blog is very good at giving an aerial view of the economy. Word to the wise, prepare for the worst and hope for the better.

Christina,

One of the small businesses I use for printing sent me an email today “you can pick your flyers up at the Kirkland office, but we no longer have any staff there.”

While I do not read Mish’s blog (feel free to post a link to that for others who read the comments here) the last line of my post is quite similar to his/her message.

“In other words…

OK, I did the calculations for Seattle and yes 44% down from the peak would be normal for our area. Let’s say we dropped 22% so far, so we have another 22% to go, just to put us at evens.

Seattle Real Estate appreciated at the rate of approximately 9.3% per year between 1997 to 2007, on average. 4% is more normal, and honestly that may be high. That leaves us with a 5.3% false appreciation in pricing, or 53%.

If I were to really think about it we added millions of housing units to our inventory in that time, prices should be dropping like a rock. I’ll research that next because they are still building, and I can’t imagine why.

Ardell,

Have you closely looked at the MLS? Sellers are still living in a fantasy world just as you were on your numerous “bottom” calls for Seattle RE. Many are still asking to break even on their 2007-2008 purchase prices or looking to get out with a 2-5% haircut. News flash, they purchased at the height of the greatest RE bubble in history. 22% is a conservative figure, imo.

AB,

I have only had one “bottom call” and that was in February of 2009 and to date prices have not been lower so that is still the current “bottom”. I don’t disagree with you at all about asking prices and sellers, and have said as much here in the comments in talking with other people.

I understand your frustration with the market, but no need to take out your arrows and point them at me. When I called that bottom the comments at the time were “let’s see where we are 9 to 18 months from now.” Well, here we are…15/16 months from then and that, my one and only bottom call, is still holding. The call was at $362,700 and median prices have not been at or lower than that to date. So my bottom call was indeed “correct” and the market has to drop another 4.3% before it is even an issue.

I posted all of that data in the RAW DATA chart, and still people come around with no supporting data to the contrary to simply act as if it were not correct when it was.

Someone explain to me why that is? I truly don’t get it.

1) I made ONE “bottom call” in Feb of 2009 saying prices would stop their rapid decline at that point and that contracts from February that would be closing in March would be “bottom”

2) To date in hindsight that was correct

My current thoughts are this:

http://www.realtown.com/Ardell/blog/seattle-real-estate/seattle-home-prices-to-go-down-43-by-year-end

I will be more than happy to talk about my predictions and forecasts being incorrect on the day that they prove to be incorrect. But until that day, let’s stop acting as if the data doesn’t prove me to have been 100% correct, because that is just not true.

Ardell:

Not sure which statistics you are using to support your claim but, at best, your bottom call is holding on by a thread. I see your bottom as already breached. I looked at realtor.org for Median sales prices in Seattle-Tacoma-Bellevue. They list median for start of 2009 at 306.2, Q1 2009 at 315.2, but Q1 2010 is already at 302.6 and trending down hard from the dead cat bounce in early ’09.

http://www.realtor.org/wps/wcm/connect/497de980426de7ccb96eff03cc9fa30a/REL10Q1T_rev.pdf?MOD=AJPERES&CACHEID=497de980426de7ccb96eff03cc9fa30a

If you’re cherry picking your stats, using only the Eastside or just metro Seattle, perhaps you’re call is still valid.

AB,

Here you go…no “cherry picking”. King County Median Home prices not including condos.

http://www.realtown.com/Ardell/blog/tracking-the-market/can-seattle-home-prices-go-down-another-22-cont

I wouldn’t go to a National Association of Realtors site for local home price information and I double check on Seattle Bubble and Redfin blog to make sure my data is not out of line with their reports of median home prices.

I very much appreciate your coming back to talk about this. More importantly it seems you are more frustrated with the fact that sellers are not ASKING that bottom or anywhere near it! On that I feel your pain.

In fact I am preparing a post and chart on the difference between sellers who are ready to sell and those that are not. It must be very frustrating to look at nice homes on the internet…pretty pictures, great house…only to find that the seller is off their rocker and asking $100,000 more than current value!

That is what I read in your comment more than you poking a stick at me as a result…”bottom” is great, but only if sellers price there…and most homes for sale are priced way, way above that. The magic number seems to be $100,000 over market value.

A wise broker once told me that $100,000 is the most common “want” of sellers. They want to walk away with $100,000. It’s amazing how often that is the case and how many sell after a $100,000 price reduction.

Fair enough. But it may surprise you to find out I am not a frustrated potential buyer. In fact, I was a purchaser during the inflating bubble. I bought in Nov. 05. Since then, I have come to the reality that it was a big mistake. However, I am honoring my obligation and not walking away. It was our first home purchase, and we felt pressured by all the hype coming from the media and particularly the RE industry.

Nothing personal against you, but I have virtually no respect for anybody in the RE industry. There’s an inherent conflict of interest for agents. Show me one agent that turned down a sale or instructed clients not to purchase in 06-07. In fact, it was a feeding frenzy for the RE industry.

I know that the entire country was, and is still in, an inflated asset bubble fueled by debt. These macro economic problems ensure your bottom call to be violated in a big way, imo. I also watch several other markets where I have friends and family living. The sellers in Seattle, for some reason, fail to grasp reality. The short sales are coming out of the woodwork. If there’s one significant round of layoffs from Boeing or Microsoft, prices could drop another 10% virtually overnight.

AB,

Interesting…well yes I will show you one agent who took a 6 month job as a Broker on salary for the second half of 2007 while I was figuring out what the new lending guidelines would do to home values. I told most every person who called me not to buy a house in late 2007 and all of 2008. Most of my calls in 2009 and to this day (got one yesterday) are people I sent away a year or more ago who are now asking me what to do next.

Yes…I sold my own house as a result of telling people not to buy…but that’s how it goes. No biggee. So if that doesn’t “gain” your respect, well then I don’t know what will.

I have already noted that my bottom call of 2/2009 WILL not hold past year end 2010. No one can forecast a “forever” result. Each year or two you have to re-evaluate based on conditions of the time, and I am calling for a 9.3% drop from here (which would take us to 5% under my own “bottom call) by year end 2011, and further declines by end of 2012 based on layoffs as you have stated.

I also do not think home prices will be back to 2007 levels until 2018 based on my studies of the previous housing market recession in 1990 or so.

Never do I talk someone into buying a house…I do not go out looking for people to talk into buying a house. People come to me and tell ME they want to buy a house, not vice versa. Sometimes it’s a good idea for them to do that, and sometimes it is not. And I am very honest in telling them what I think. That’s the best I can do. Many times when I caution people not to buy or not to buy a certain house, they appreciate my honesty but buy it anyway. It’s a free Country that way.

I sold homes in 2007 and 2008 without ONCE asking if the seller wanted to buy a replacement home. If they tell me that is what they want to do…OK. But I didn’t even ask them that question.

I sold a client’s home in November of 2007….the seller of that home just called me a couple of months ago and just bought a house two weeks ago. I never once called her in between to ask if she was “ready to buy a house”.

Here’s one for you. In April 2005 (before the big upswing of 2005) a young man and his parents came to me to buy a condo, which he did by June of 2005. I contacted him and his family five or six times when he owned it for exactly 2 years in June of 2007. The condo had doubled in price. He was 19 when he bought it and 21 when I BEGGED him to sell it.

He said he liked where he was living. I said take that $75,000 or more tax free gain and put it in your pocket and rent in the same building for $700 a month. He said, I really like my place so no I don’t want to do that.

So maybe your comments are generally correct…I don’t know. But I clearly don’t deserve to be painted with the same brush you are painting “all agents” with…and maybe they don’t either. Did your agent pressure you into buying? Did he/she come to you in 2005 or did you go to him/her? I don’t know. You tell me.

Look Ardell, we all appreciate how you finally saw the light and recognized the oncoming pain in the RE market, but don’t pretend you were somehow ahead of the curve and telling everyone to stay away. If I recall correctly, you fought tooth and nail until sometime in 2008, and by then, what was going on was apparent to everyone but the most ridiculous of Seattle-PI RE bloggers (hey Mack McCoy! we need an update to that Bubble-Blogger Rap.).

I’m trying to find some posts of yours that are warning readers back in 07, could you link me to some? I did find one post in late 2007 trumpeting appreciation that had “nothing to do with loose lending standards.”

This is going to sound really snarky but it’s an honest question: if you have had such a keen eye for the RE market the last 3 years, why did you sell your house for $300,000 less then you paid (and basically waiting until just after your own “bottom call” to do it)?

Excellent question(s), Reid.

Reid said/asked: “Look Ardell, we all appreciate how you finally saw the light and recognized the oncoming pain in the RE market, but don’t pretend you were somehow ahead of the curve and telling everyone to stay away. If I recall correctly, you fought tooth and nail until sometime in 2008, and by then, what was going on was apparent to everyone but the most ridiculous of Seattle RE bloggers.”

Reid, here is a post of mine from late 2007:

http://raincityguide.com/2007/12/13/should-you-buy-a-short-sale-property/

In the post above I talked to people about buying short sales in late 2007. When the market is positioned to go down, and you still want or need to buy a property, you may have to jump ahead of current market price by buying a home at tomorrow’s lower price. So the integrity of being a real estate agent is in helping someone do what they want to do (buy a house) as best they can.

Yes, I can tell some and maybe most clients not to buy at that time. But that is not necessarily an option for ALL clients. Most of my clients are not buying a home to make money or to lose money. They are buying a home to get closer to work or because they are having a baby or their mother is ill and needs to move in and they need more space. Each client has to weigh the odds of price going down with their compelling reason to buy… that compelling reason having nothing to do with money in most cases. If they must buy a home, and some people do regardless of market conditions, I can say well let’s try to find a home at less than current market value (a short sale as example), so that when the market goes down, you will be ahead of the curve.

By choosing to write on the topic of Short Sales…I am acknowledging that buying at tomorrow’s lower price may be a reasonable alternative IF one needs to buy a home right now.

Sometimes you have to read between the lines. You say I didn’t tell everyone to “stay away”. Sometimes you have to watch what I’m doing vs. what I’m saying. The earliest concrete evidence of the market change here in the Seattle Area was August 3, 2007. Prices were not yet impacted, but the handwriting was clearly on the wall on August 3, 2007 moreso than July 20, 2007. So how do I maintain my integrity? I don’t SAY “stay away”, I lead by my actions vs my words:

http://raincityguide.com/2007/08/26/ardell-con-brio/

I went away…I stopped blogging as much…I took a salaried job for 90 days…and then another 90 days…so I could sustain myself without needing to tell my clients to buy. I blogged that shift in what I was doing. I told my clients who could wait to buy…to wait…and I also waited on the sidelines as an agent to some degree, by using that time to train agents vs. selling houses. I continued to blog…but not here and not to consumers. I started a Blogging Broker blog someplace else where agents read primarily and limited my training to how to be a better agent during the hiatus NOT how to “get” more clients to “sell to”. I focused the agents on helping sellers sell vs helping buyers buy, and told them it was a better time to sell than buy, so focus on sellers and not buyers as much as possible. I even told one of the agent’s clients not to buy…that didn’t go over well 🙂

I continued to help people sell, because it was a good time to sell, and supplemented my income with a salaried position. The integrity of an agent is shifting to mostly sellers when it is a better time to sell and shifting to mostly buyer clients or half sellers/half buyers when it is a good time to buy.

Sometimes you have to read what I am doing. I can’t tell everyone else’s clients what to do…I can only tell my clients what to do…and I don’t always do that in a blog post. Sometimes I do and sometimes I don’t and sometimes I say it encryptedly for those who are paying close attention.

By “sitting out the game” on the sidelines…I am saying “Hey everyone, it’s time to watch from the sidelines and decide when to get back in the game”. It’s what I did, and I wrote the above post to show people it may be a good time to sit this one out IF you are a buyer…not if you are a seller.

After sitting it out for 6 months to collect my thoughts and formulate an opinion that the market was ZOMG!!! Which you say I did not warn of and was holding on tooth and nail…read this.

http://raincityguide.com/2008/02/03/hold-on-to-your-hats-sunday-night-stats/

I sat out from 8/07 to 1/08 for the most part…and came back with the message “hang on to your hats”, prices may not be down yet, but watch the volume which is dropping like a stone! Lower volume has to eventually translate into lower prices. So I would have to say you are incorrect with regard to my not “calling it” from the get go or my not maintaining my integrity every step of the way, week by week, day by day.

Reid said: “I’m trying to find some posts of yours that are warning readers back in 07, could you link me to some? I did find one post in late 2007 trumpeting appreciation that had “nothing to do with loose lending standards.

Reid,

As a former (and future) client of Ardell’s, I followed her blog closely during the 2008 year when I wanted to sell. I can attest that the advice she provided me directly was much more frank than what was posted on the blog (which was… sell now (emphatically) even if it’s not as much as you want because it’s only going to go down from here….and quickly!). Ardell was right on the money (pun intended).

Personally, I am wondering where this criticism is originating from (and I DO find it snarky). You seem to use the idea that Ardell not actively predicting the coming drop in prices back in mid-2007 (when prices were still peaking in Seattle while the rest of the country was taking a downward spiral due to….loose lending practices!) as reason to completely discredit her current prediction. Is that what the point is?

This blog is about Ardell’s prediction about what she thinks will happen in the future, and she is making certain assumptions to arrive at those predictions. Predictions ARE educated guesses. There is no guarantee that predictions will come true. More importantly, any changes to those assumptions result in a change in those predictions. So, while Ardell assumes that a top employer will go through a round of layoffs which will result in a 10% drop in prices, this is an assumption that may or may not come to fruition. If the layoffs never come, then prices might drop only 5%. If layoffs are more significant, then prices could drop more. In late 2007, the lending industry choked almost overnight. If I remember Rhonda’s blogs correctly, that blow was much more sudden and severe than anyone was expecting (even for those who were expecting the pendulum to start swinging towards more conservative loans). So, the old predictions were based on old assumptions about lending. New lending practices = new assumptions = new predictions. Old predictions go out the window.

My point is you should be evaluating her assumptions and predictions with the available data we have NOW. Using her “lack of a 2007” call for the situation we are in mid-2010 as the foundation of your disagreement is simply not logical as it has zero influence on her current model.

Thanks Leslie. I appreciate your kind words.

The odd thing about the run up is those “loose” lending standards, to some degree, were always available for as far back as I can remember. Interest only mortgages were around as were stated income loans 20 years ago. So “loose lending” was not a new thing at all…what was “new” was the volume of people using them vs. the use for which they were originally intended and always utilized, sparingly.

There were times when I felt it was crazy. But there were other times when I thought, well only wealthy people used interest only in the past, and only small business owners used stated income in the past…so maybe the secret just got out to the masses. Maybe the poor started figuring out what the rich already knew.

So yes, I knew loose lending was running the market up, but no I did not ever guess the day or even that there would be a day, when that loose lending would cease. To me those “exotic” loans were not new at all, only the surprising number of people using them.

The real issue, which no one talks about, is that the lenders chose to be uninsured via PMI. The lenders wanted high interest rate 2nd mortgages instead of PMI (private mortgage insurance). They gambled that getting higher interest was better than being insured…they turned out to be wrong. But that’s a long story that no one seems to want to notice. Everyone wants to blame it on the borrower…but it is not the borrower that failed…it was the lenders choice not to be insured on the top 20% of the value that failed. They would have been “bailed out” by the insurance companies, the same as they always were in recession periods. This time they needed a government bailout, because they kept the high interest payments, but didn’t want to pay for the risky decision to be uninsured.

The taxpayers get mad at the borrower…but if there was PMI, the rest of the country would not have been involved…nor would they likely have noticed as much. They certainly wouldn’t have gotten angry if the insurance companies took the hit…vs them. That is the difference in this recession vs the last one. No PMI.

Ardell, thank you for the honest answer to my questions.

I’ll admit it was a bit of a personal interest because you were so free in telling your “sub-prime” story to start, but then we never got an answer to the ending.

In the years I’ve been reading Seattle RE blogs, you’ve been a bit of a lightening-rod online (well, probably more than a bit), but you have always been on my short list for agents who I don’t doubt bring real value to the client.

Ried,

You are very welcome. I posted “the ending” here and there, but not in a blog post. When I first “sold” the house for slightly less than I paid, I was not behind in my payments and it was over a year before the closing date you are seeing. But to get a short sale approved, you have to be behind and almost to foreclosure. That’s why things turned the way they did. It’s just the game the banks play and sometimes you have no choice but to play their game. I’m not saying it was a strategic default…just saying the lender would have been much better off if they had trusted my opinion and accepted the offer I brought them in April of 2008 vs taking a much lower one over a year later.

I don’t highlight the story in a blog post because I have a partner in all things and he is entitled to a bit of privacy. I on the other hand stick my neck out there, and honestly, I’m surprised it doesn’t get chopped off more often. People are generally very respectful and kind to me, and I appreciate it.

Something I don’t talk about often is I truly believe that my experiences help me be a better counselor to the people who need my assistance. I have been able to bring comfort and useful information to many, many people, by having gone through it myself. It makes me a better agent the same way that personally having gone through a corporate relocation a couple of times with my children, helps me assist relocating families better. Somewhat like a “method actor”, walking the walk helps you guide others in their walk, and so it’s “all good” in the end.

I appreciate your last paragraph, and in the 20 years I have been doing this (real estate agent; not blogging) my clients have agreed. I would not have stayed in the business this long if they didn’t.

Watch the Dow, people. It’s your Macro indicator. Took a nose dive today to below 9,900.