Rhonda Porter is an NMLS Licensed Mortgage Originator MLO121324 for homes located in Washington state. Her blog, The Mortgage Porter, is nationally recognized for sharing relevant information to consumers about mortgages.

She has been originating mortgages since 2000 at Mortgage Master Service Corporation #40445 Consumer NMLS Website: http://www.nmlsconsumeraccess.org/TuringTestPage.aspx?ReturnUrl=/EntityDetails.aspx/COMPANY/40445

NMLS ID 40445. Equal Housing Opportunity.

You can follow Rhonda on @mortgageporter, Facebook and/or Google+

Fannie Mae recently launched KnowYourOptions.comto help struggling homeowners who may be feeling overwhelmed with their mortgage situation. The website is gearred towards avoiding foreclosure and warns homeowners not to walk away from their home.

The site features interactive tabs:

Options to stay in your home

Options to leave your home

Resources

Beware of Scams

Take Action

There are calculators, videos, checklist and forms for home owners to check out.

With regards to the refinance section under “options to stay in your home”, know that you may not have to go through your mortgage servicer (who you make your mortgage payments to) with the home affordable refinance. Your local mortgage originator may be able to help you with your home affordable (or any) refinance.

UPDATE TO POST 10:15PM: If you are considering leaving your home, before you decide on a short sale, deed in lieu or foreclosure, please contact an attorney. Fannie Mae’s site insinuates that with a foreclosure you may have a deficiency judgement–opting for a short sale or deed in lieu of foreclosure does not guarantee that you will not have a deficiency judgement (depending on your personal scenario).

The term “mortgage broker” has become bastardized in recent years by the media and our elected officials in Congress. The term is often wrongly used to describe a mortgage originator who’s gone bad or done something wrong. Mortgage brokers are blamed for what’s gone foul in the mortgage industry when the room was packed with mortgage originators who work for banks, correspondents and credit unions…it’s just so much easier to blame the dog.

Yesterday, when Jillayne wrote a post about Shawn Portmann, the Seattle PI originally has the title to their article incorrectly calling him a “Mortgage Broker”; after the Washington Association of Mortgage Professionals contacted the author, he corrected the title to read: “Feds to mortgage banker: We want your giant bag of money”. I considered this a small victory for WAMP and applaud them for getting the Seattle PI to correct their title and for defending the mortgage industry.

I wasn’t so lucky last spring when I tried to get the Seattle Times to correct calling a mortgage orignator who worked for Chase Bank a “mortgage broker“…you might remember the story involving stated income loans for hot dog vendors and limo drivers from Russia who were trying to sue Chase for hundreds of thousands of dollars over their lost earnest money. She refused to correct her article. How an employee of Chase is a “mortgage broker” beats the heck out of me.

It’s very convenient for big banks to vilify “mortgage brokers” because somehow they believe it makes their mortgage originators appear to be of a higher quality. And….once the small mortgage broker industry has reduced to almost nothing, consumers will all have to go to one of three banks or a handful of remaining correspondent lenders or credit unions for their mortgage needs.

The big bank$ have convinced Congress that it is the “mortgage broker” who has smelled up the industry. Somehow they forgot to mention that:

mortgage brokers only sell bank products and programs. Wholesale bank reps call on mortgage brokers and correspondent lenders begging for our business. Back in the subprime days, they’d be lined up out my door pushing Countrywide, Washington Mutual or World Savings/Wachovia option ARMs stated income or 100% financing. These programs were created by the banks/lenders not brokers. The broker was the street dealer (sales) and the bank was the drug-lord/meth-lab (supply).

mortgage banks/wholesale lenders underwrite the loans that brokers originate for the bank. Brokers do not make underwriting decisions–mortgage banks do and correspondent lenders do can (per bank guidelines). If a wholesale lender/bank did not want to make a loan sent to them by a mortgage broker–they could decline it!

“Mortgage brokers will be prohibited from making higher commissions by selling mortgages they know consumers can’t afford.”

First of all, I agree that NO mortgage originator, regardless of the type of institution they work for, should earn a higher commission for selling inappropriate mortgages–in fact, they should not originate that loan <period>. This point is so poorly written — is it saying that a mortgage banker CAN make a higher commission originating bad loans? Our own White House has joined in on bastardizing the “mortgage broker”!

My plea is that Congress and the media use the term “mortgage originator” when in doubt of what type of institution the MLO is employed by or if they’re making a general statement about mortgage originators. The definition of “mortgage broker” is not an unsavory mortgage originator. This is reckless to an industry that is fighting to stay alive.

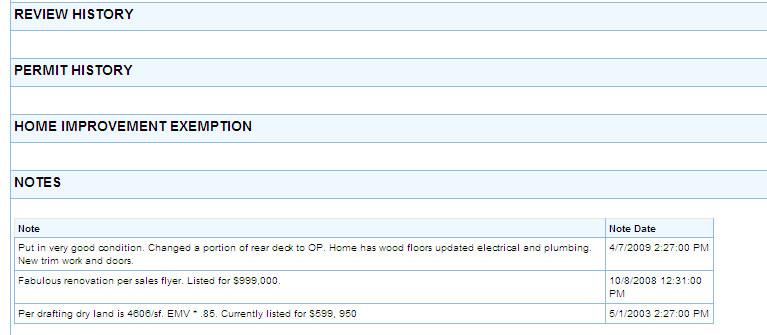

The King County Tax Assessor’s office recently added the photos they have available on line. It’s a pretty cool feature where you can possibly see the history of your home. I wrote a post showing old photos of my former home on North Lake in Auburn and how to obtain the King County Tax Assessor’s photos. However, I learned today is that the King County Tax Assessor’s office is also making note of the asking price on listing flyers and the comments are available on line under the “property details” section.

Check out how it’s noted on October 2008: “Fabulous renovation per sales flyer. Listed for $999,000“. This is not my home but I have knowledge of it and I can tell you that it never sold for anywhere close to that…in fact it never sold.

It’s amazing to me that King County is looking at listings and making notes such as this about any property. Sure enough, the following year, this property’s tax assessed value increased by just shy of $100,000 (or 12%).

Did the listing flyer impact the tax assessors opinion of value on this home?

All mortgage originators who work for mortgage brokers or correspondent lenders/consumer loan companies must be licensed with the NMLS as of July 1, 2010 to take a residential loan application for property located in Washington. If your mortgage originator works for a bank or credit union, they only need to be registered with the NMLS (which means “do nothing” at this point).

Last Friday, Deb Bortner, Director of Consumer Services for Washington State’s Department of Financial Institutions, issued this statement:

“Unfortunately, many applicants did not submit by the deadline. I want to assure you that, even with the current budget reductions and staffing constraints, our Licensing Team is doing all it can to balance a timely review while complying with the recent provisions of state and federal laws that are designed to provide increased consumer protection. While we will process as many applications as possible by July 1st, we will not be able to fully address the volume of late applications that we are currently receiving.

It is important to remind each member of the industry that on July 1 an individual may not act as a Mortgage Loan Originator unless he/she is licensed or has received official written e-mail communication from DFI outlining the conditions under which that individual can work…”

It’s unfortunate for consumers that Congress made two separate classes of mortgage originators: Licensed and Registered. You can follow the dollars to figure out how that happened. In my opinion, all mortgage originators should be held to the same standards. Consumers should not have to determine whether a mortgage originator is licensed or not and what licensing means verses a simply registered mortgage originator working for a bank mortgage company or credit union. With that said, I’m thankful to be in the licensed category since those LO’s who are licensed are held to a higher standard than a registered loan originator per the SAFE Act.

Tomorrow, many mortgage originators employed at consumer loan companies/correspondent lenders or mortgage brokers who did not jump through the licensing hoops quick enough will either need to cease taking applications or go work for a bank or credit union. Again, this is for residential mortgage applications on properties located in Washington State (this applies to mortgage originators not in the State of Washington but taking applications on residential property located in Washington).

You can verify if your mortgage originator is licensed by checking http://www.nmlsconsumeraccess.org . You can run a search by entering their first and last name along with the state abbreviation. If your mortgage originator works for a bank or credit union, they’re not required to be licensed and registration is not available for them yet.

As of this moment, I still haven’t heard if the Senate has passed an extension for today’s deadline for transactions to close and still qualify for the Home Buyer’s Tax Credit. Even if the Senate is successful in passing this hot potato the House has lobbed at them, everyone in the industry is inundated with transactions that are suppose to close today. Everyone will still be trying to honor the contract’s closing date.

My title insurance sources tell me that in a “normal” month, 1/5 to 1/4 of their revenue takes place on the last day of the month. Imagine how this has been magnified with the June 30th deadline for closings.

I’m suggesting that if you can wait until tomorrow to call or request something from your escrow and title partners, please do. Many companies are not “over staffed” due to our economy.

This mostly impacts the real estate professionals who are on the “closing end” of the transaction. For real estate agents and mortgage originators, it’s probably business as usual. 🙂

This is an email that I received last night with a bank using the fact that mortgage originators who are employed by a depository bank or credit union are not required to maintain a license. Here’s more from the email:

[Big] Bank has been in the industry for over 100 years. As one of the nation’s top federally Chartered banks, [Big] Bank has the size and depth of the larger banks with the mindset of customer service being our #1 priority!

If you are an experienced loan originator looking for a change, HERE IS YOUR OPPORTUNITY!!!

What more can you ask for? Do NOT miss this opportunity to take your career to the next level.

Am I surprised to see a bank use the fact their mortgage originators are not licensed as a recruiting tool? Not really.

I’m sure they feel it’s a great advantage to not have to be held to the same standards as Licensed Mortgage Originators (passing state and national exams, continuing education, financial stability of the LO, etc). Banks probably believe that consumers don’t care if the mortgage originator has satisfied what is required of a licensed LO per the SAFE Act–because they’re employed by a big bank and somehow, that makes the consumer safe.

I’m wondering what type of mortgage originator would say “Hey, I don’t want to have to take the exams, have my credit history checked or do NMLS certified continuing education…I’m going to work for a bank or credit union!‘

Consumers: Does it matter to you if the person helping you obtain your mortgage is licensed (held to a higher standards per the SAFE Act)? Or if they work for a big bank or credit union, and are merely “registered”, is that good enough for you?

It’s no surprise that the Federal Reserve left the funds rate at the current lows of 0 – 0.25% on the heals of continued weak housing data. What investors are looking for is “what” is being said in the FOMC Statement that is released in conjunction with their rate decision.

If you have a home equity line of credit that is tied to the prime rate, your rate should be unchanged (for now). Otherwise, this decision does not have a direct impact on mortgage rates. It does influence the markets (stocks and bonds) which impacts mortgage rates.

Household spending is increasing but remains constrained by high unemployment, modest income growth, lower housing wealth, and tight credit….employers remain reluctant to add to payrolls. Housing starts remain at a depressed level. Financial conditions have become less supportive of economic growth on balance, largely reflecting developments abroad. Bank lending has continued to contract in recent months….subdued inflation trends, and stable inflation expectations, are likely to warrant exceptionally low levels of the federal funds rate for an extended period.

Prior to the FOMC Statement, mortgage backed securites are flat (but still at record levels with very low mortgage rates). Follow me on Twitter to see live rate quotes. If I have intraday rate changes today, I’ll update this post.

Effective on loan applications taken on June 1, 2010 or later, Fannie Mae is requiring lenders to confirm that undisclosed liabilities are not present prior to funding a transaction as part of their Loan Quality Initiative (LQI). Currently a credit report is pulled and is valid for a specific amount of time–as long as the transaction closes prior to the expiration of the credit report, it typically is not repulled. Fannie Mae is now requiring the lender to make sure that there is no new or undisclosed credit at closing. Relying on the original credit report pulled at application is no longer good enough.

Fannie Mae’s FAQs suggest these tips for lenders to help confirm there are no undisclosed liabilities:

Retrieving a refreshed credit report just prior to the closing date and reviewing it for additional credit lines.

Utilizing new vendor services to provide borrower credit report monitoring services between the time of loan application and closing.

Direct verification with a creditor that is listed on the credit report under recent inquiries to determine whether a prospective borrower did in fact obtain credit or enter into a financial arrangement that is not disclosed on the loan application.

Running a Mortgage Electronic Registration System (MERS) report to determine if the borrower has another mortgage that is being established simultaneously.

This means days before funding a Fannie Mae loan, the transactions are subject to being re-underwritten and if the borrower is “borderline” (which is a 620 mid-credit score in today’s climate and/or higher debt-to-income ratio) or decides to purchase their appliances for their new home before closing…they could potentially “kill” their deal and find themselves being “unapproved”.

Fannie Mae states that loans should be resubmitted to underwriting if:

additional debts have been incurred which would increase the debt-to-income ratios

if new derogatory information is detected

if the credit score has materially changed

Borrowers should understand that the loan application is intended to represent their financial scenario and whenever (even before LQI) changes are made to their application, their mortgage originator needs to know. This is not new. When changes occur and a borrower is aware (such as taking on more debt or changing their employment) and they hope they “won’t get caught” before closing, they’re committing fraud. This is what Fannie Mae is trying to prevent with LQI.

Borrowers with conventional financing need to be extra mindful of LQI. Using a credit card to fill your SUV full of gas could potentially ding your score if you’ve carry a balance of 30% or more of the available credit limit. Even closing a credit card during or just before a transaction could drop your score low enough to where the lender may have to reconsider your loan approval AT CLOSING.

For mortgage companies and banks (anyone who sells loans to Fannie Mae) it boils down to having to refresh, repull or face re-purchasing the loan if changes to the credit report are found between application and funding. Fannie Mae is not specifically requiring credit reports be repulled prior to funding–they are holding the lender responsible for changes if they don’t.

Borrowers, real estate agents and originators need to be prepared for potential delays in closing, repricing of their mortgage loan (which would trigger another delay due to MDIA) or the loan potentially being denied. It’s more important than ever that borrowers work closely with a qualified mortgage professional who can help guide them through the process.

I recently received this question from a Rain City Guide reader:

I wanted a GFE from my lender… but am told I can only get one if I lock in the rate. Is this legal?

Effective January 1, 2010, a Good Faith Estimate is required to be issued no later than 3 business days once a mortgage originator has received all of the following:

borrower’s full names

monthly income

social security numbers to obtain a credit report

property address*

estimated value of the property

loan amount

any other information deemed necessary by the loan originator to complete an application

The above items are how HUD defines a loan application. One item that can be a bit tricky for consumers and loan originators alike is the property address. Yes, a mortgage origiantor can issue a Good Faith Estimate without a property address, however IF they do, it’s at a substantial risk.

From HUD’s RESPA FAQs (April 4, 2010 edition) 33:

…a GFE issued without a property address, the future receipt of the property address is not a changed circumstance that would allow the loan originator to issue a revised good faith estimate.

This means that the Mortgage Loan Originator would be on the hook for fees that are outside the specific tolerances set forth in the HUD’s Good Faith Estimate if a MLO issued the GFE without a specific property address. I think this is something that HUD needs to take a serious look at this if they truly want the Good Faith Estimate to be a shopping tool for consumers–otherwise, the “shopping” process can only take place after the borrower has identified their next home.

From HUD’s RESPA FAQ 23:

An application includes information the loan originator requires the borrower to submit in anticipation of a credit decision. If a loan originator issues a GFE, the loan originator is presumed to have received all six pieces of information.

A mortgage loan originator CAN issue a good faith estimate without the rate being locked. Going from a “float” (unlocked) to a locked rate constitutes a “changed circumstance” which allows the MLO to re-issue a good faith estimate. In fact, the GFE must be reissued withing 3 business days of the locked loan and any interest rate dependent changes may be reflected on the revised GFE.

HUD’s RESPA FAQ 31:

…a loan originator may not require a borrower to sign consents to verify employment, income or deposits as a condition of issuing a GFE as such a requirement may inhibit borrowers from shopping for the best loan by leading borrowers to believe that they are committed to obtaining a loan from that loan originator.

If you have provided all the information stated above to complete an application, including a property address, your mortgage originator must either issue a good faith estimate within three business days or deny your application. If they do not, they are violating RESPA.

WaMu’s pay system rewarded loan officers for the volume of loans they closed on. Extra bonuses even went to loan officers who overcharged borrowers on their loans or levied stiff penalties for prepayment, according to the report of the Senate panel’s investigation.

“Washington Mutual engaged in lending practices that created a mortgage time bomb,” Levin said. “Because volume and speed were king, loan quality fell by the wayside.” …

In some cases, sales associates in WaMu offices in California fabricated loan documents, cutting and pasting false names on borrowers’ bank statements, the panel found. The company’s own probe in 2005, three years before the bank collapsed, found that two top producing offices – in Downey and Montebello, Calif. – had levels of fraud exceeding 58 percent and 83 percent of the loans. Employees violated the bank’s policies on verifying borrowers’ qualifications and reviewing loans…”

“Washington Mutual and Long Beach compensated their loan officers and processors for loan volume and speed over loan quality. Loan officers were also paid more for overcharging borrowers – obtaining higher interest rates or more points than called for in the loan pricing set out in the bank’s rate sheets – and were paid more for including stiff prepayment penalties…”

The difference between mortgage bankers and mortgage brokers compensation is that mortgage brokers are the only one’s who are required to disclose how they’re compensated on the “back end” (yield spread premium).

James Vanasek, former Chief Credit Officer and Chief Risk Officer seemed relieved to have a chance to tell the subcommittee how his attempts to right Washington Mutual were ignored from management. From his submitted testimony, he feels that Washington Mutuals tagline sent the wrong message to their mortgage originators: the “Power of Yes” absolutely needed to be balanced with “The Wisdom of No.”

“Because of the compensation systems rewarding volume vs quality and the independent structure of the loan originators, I am confident that at times borrowers were coached to fill out applications with overstated incomes or net worth adjusted to meet the minimum underwriting policy requirements. Catching this kind of fraud was difficult at best and required the support of line management. Not surprisingly, Loan originators constantly threatened to quit and go to Countrywide or elsewhere if their loan applications were not approved.”

Washington Mutual was one of the pioneers of the option ARM, offering this product as far back as the 80s (per Killinger’s submitted testimony) I remember back in the 90’s participating with a Washington Mutual loan originator who was presenting the product to a group of investors. This use of this product made more sense than how they (and many others) wound up pushing it.

Our company actually banned this product and I know we lost business by not providing option ARMs if we could not convince the borrower to use a more fixed loan. Account executives from every bank who had an option ARM would be sure to let us mortgage originators know just how much income we were losing. I was (and am) okay with that.

From Senator Levin’s opening statement:

“WaMu was eager to steer borrowers to Option ARMs. Because of the gain from their sale, the loans were profitable for the bank, and because of the compensation incentives, they were profitable for mortgage brokers and loan officers. In 2003, WaMu held focus groups with borrowers, loan officers, and mortgage brokers to determine how to push the product. A 2003 report summarizing the focus group research stated: “Few participants fully understood the Option ARM. … Participants generally chose an Option ARM because it was recommended to them by their Loan Consultant….

To increase Option ARM sales, WaMu increased the compensation paid to employees and outside mortgage brokers for the loans, and allowed borrowers to qualify for the loan [based on a minimum payment]…”

Adding to the problems, WaMu and Long Beach Mortgage frequently steered borrowers who qualified for prime loans into subprime loans, the subcommittee found.

This post is all ready too long to discuss Long Beach Mortgage…but I can’t help but share this point I’ve tried making several times about what happened time and time again with Account Executives from banks (not just WaMu) who called on mortgage brokers to push the bank product (from Huffington Post):

“Within Long Beach Mortgage, former employees described how some sales people taught brokers how to break the rules, including using fake and forged documents.”

I’m glad to say I never sent a loan to Long Beach Mortgage and somehow I managed to only send one loan to Washington Mutual (which was an interesting story in its own).

Fannie Mae recently launched KnowYourOptions.comto help struggling homeowners who may be feeling overwhelmed with their mortgage situation. The website is gearred towards avoiding foreclosure and warns homeowners not to walk away from their home.

Fannie Mae recently launched KnowYourOptions.comto help struggling homeowners who may be feeling overwhelmed with their mortgage situation. The website is gearred towards avoiding foreclosure and warns homeowners not to walk away from their home.