The #1 Question in Real Estate is “How Much is THIS Home Worth?”

Every single person who is buying a home or selling a home is going to ask that question. Most people doing a refinance need the answer to that question as well.

1) A home seller needs to know the highest possible price they can sell for.

2) A home buyer needs to know the lowest possible number than can “get it” for…BUT they also need to know the maximum amount they SHOULD pay for it. The answer is often not one in the same.

3) A person planning to refinance, needs to know how much an appraisal will say it is worth, which isn’t necessarily the same method of valuation used by home buyers and home sellers.

Why do you need to know that Home Prices in King County are at early 2005 levels? Because that fact should lead you to some generally true conclusions.

1) If you are a seller thinking about selling your home, and you bought it between 6/2005 and 12/2008, you would be starting from the assumption that you CAN’T GET WHAT YOU PAID FOR IT”. If you bought it in 2001 and never refinanced it, then you should be able to sell it and walk away with positive net proceeds.

2) If you are a buyer wondering what to offer against the seller’s asking price, and he is asking more than he paid for it in 2007…well…you probably need to walk away. Maybe not see that home in the first place.

3) If you are thinking about refinancing and you bought the home in 2007 with zero down, you likely can’t. So save yourself the cost of trying.

Are there exceptions? Well, only a fool says never or always. But if you think you ARE the exception, you better have a really, really good reason why.

I know…your house is different. Your neighborhood is better. REALLY? Usually not as much as you think.

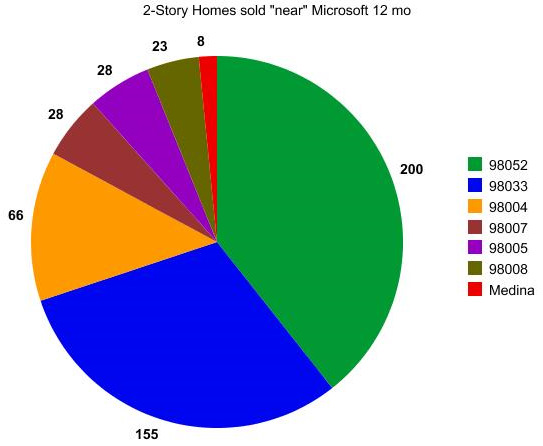

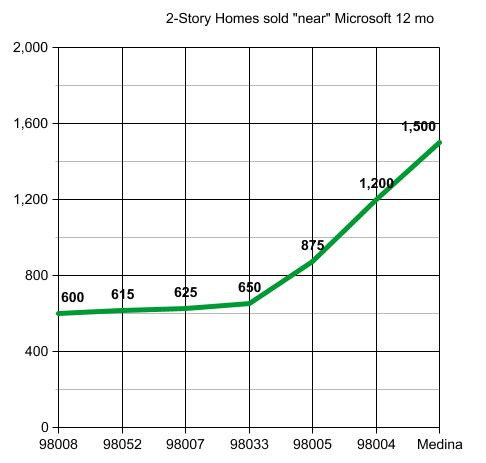

A good example of the dangers of applying Home Sale Statistics improperly, is in Redmond.

The Median Home Price in Redmond is up 66% from 2001 to Present, but not THAT house. That’s why you need to know when an area is running much higher or lower than the overall County market stats, and WHY.

Overall median price in Redmond is up 66% from 2001. Based on that true fact”:

1) A seller (erroneously) lists his home at 66% more than he paid for it in 2001. The house was built in 1985. He paid $350,000 + 66% + “negotiating room” = $599,950. He lists it at the highest possible price he can “reasonably” get for it. And he wants at least $575,000. This based on an article he reads saying Median Home Price in Redmond is up 66%, which is true…but not for HIM.

2) A buyer who reads my blog sees that 66% only applies if you include homes built in or after 1990. He sees that the % increase for homes built in Redmond prior to 1990 carry a median price of 42% more than 2001, vs 66% more. So while the “lowest price” the seller will accept is $575,000, the highest price he might be willing to pay is $500,000. We’d need to test homes built in the 80’s vs ALL homes built prior to 1990 to know for sure what a “reasonable” price for that home would be.

3) A person refinancing may expect it to appraise at $580,000, using the same logic as the seller in 1) BUT the appraiser may come up with $550,000 based on “3 comps”. This assuming the “average buyer” will pay closer to what the seller wants, than what the property is actually “worth”. An appraiser only looks at what people paid recently, not whether or not those few buyers were correct in determining “price to pay”.

There’s Good Reason why The #1 Question in Real Estate is what is THIS home WORTH?”

It’s one of the hardest questions to answer correctly. Keeping up on where home prices are generally (early 2005 levels) gives you a leg up on simply “What is the seller willing to take?”. But local stats can be misleading, if you don’t take the time to take it down to Apples to Apples.

Information is of Great Value! Knowing how to apply that information…is PRICELESS.

Under

Under