Seattle Bubble announced about a half hour ago that it is changing it’s name to Sound Housing News.

If that’s not a sign of the times…I don’t know what is. Talk about “Breaking News”!

“Seattle Bubble

Seattle Bubble announced about a half hour ago that it is changing it’s name to Sound Housing News.

If that’s not a sign of the times…I don’t know what is. Talk about “Breaking News”!

“Seattle Bubble

Buyer Beware of Real Estate “lingo”. The soft language of “making an offer” is really leading you to sign a binding contract. For some this comes as no surprise. But for others who may think they are simply making an offer, and later deciding whether or not they really want to buy the house, this is very important. If the seller signs your offer without any changes, you are in a binding contract to purchase that house.

Buyer Beware of Real Estate “lingo”. The soft language of “making an offer” is really leading you to sign a binding contract. For some this comes as no surprise. But for others who may think they are simply making an offer, and later deciding whether or not they really want to buy the house, this is very important. If the seller signs your offer without any changes, you are in a binding contract to purchase that house.

An agent can pretty much tell what is happening when the buyer is signing the contract. That is why I think all contracts should be signed in person, in front of the agent, and not via fax or e-signing. If they are only paying attention to the offer price, signing quickly, and not asking questions about or reading the 10 or more attached pages to “the offer”, it becomes fairly evident that they are thinking they are flushing out the “true” price vs. the asking price from the seller. Not so. Another clue is if the “offeror” is asking how they get their Earnest Money back, before signing the offer. In real estate you quickly move from making an offer to actually buying THAT house, in many cases. Once the seller signs that “offer” you are quickly pushed into the queue toward closing via the escrow process that ensues.

The key is not simply to leave yourself a bunch of legal outs, but to make sure that you really ARE going to buy that house, unless new information suggests otherwise. You should not be cancelling “on inspection” because you decided not to buy the house because of the street it is on, unless you learned something new about that street (from the inspector) AFTER you made the offer. You can, but you shouldn’t. You should consider that the seller is thinking that you really do intend to buy his house, based on what you could readily see prior to making the offer. Making an offer is not really a “maybe I will buy it”. Making an offer is indicating that you ARE buying it, unless new information that was unavailable at time of offer comes forth prior to closing, and during the due diligence period of the contract.

Technically you can lose your Earnest Money if you say “I changed my mind about buying a house” when you ask to cancel “on the home inspection”. Well, let’s change that to you SHOULD lose your Earnest Money if you are cancelling merely because you changed your mind, or because you didn’t realize when you made the “offer” that you were actually agreeing to buy the house. Remember, you are causing the seller to REMOVE the home from market. You are pulling the property OFF of the public portals. You should not be doing that simply to have more time to think about whether or not your really want to buy it.

Making an offer means you want to buy that house. An offer to purchase is not intended to be used simply to prevent other offers from coming in, while you think about whether or not you want to buy that house.

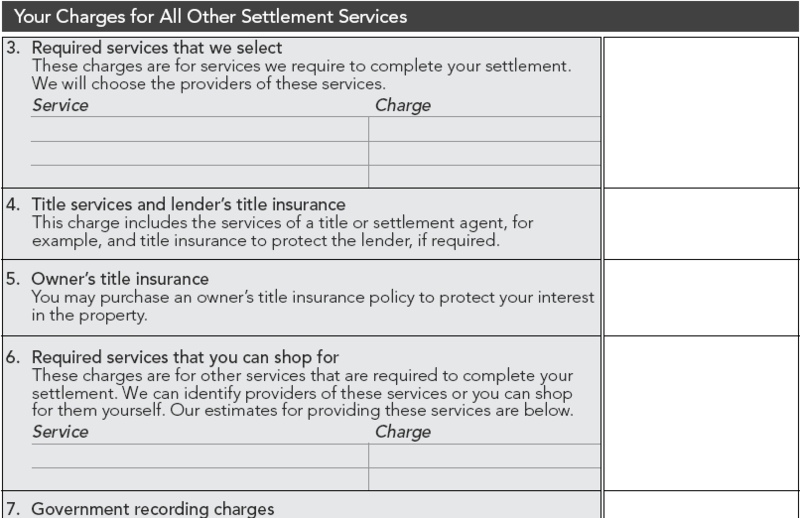

The new Good Faith Estimate will be required to be used on all new loan applications effective January 1, 2010. Part of HUD’s GFE may include a service provider list which consists of title and escrow/settlement providers (boxes 4, 5 and 6; section b on page 2 of the GFE). This list (if permitted by the lender) is important to the consumer as it will determine what the cost difference can be between the good faith estimate and the settlement statement at closing.

If a borrower relies on a service provider (title and escrow/settlement services) on the list given to them by their mortgage originator with the good faith estimate, there is a 10% tolerance. This means that if the cost at closing comes in more than 10% higher of the sum of those fees than what was provided on the good faith estimate, the lender will pay the difference (or credit the borrower) over the 10% sum of those fees. However if the lender permits and the borrower to shop for their own title and/or escrow vendor, the loan originator is “off the hook” should the fees come in higher at closing.

Per HUD “if no service providers are listed, then it is assumed the customer could not shop and fees will be bound by the tolerances” and that “lenders are responsible for fee requirements listed by their loan officers or the broker”.

If the lender “permits” the borrower to shop for title and escrow services, they must provide this written list which must include at least one service provider on a separate sheet of paper and then the lender is subject to the 10% tolerance (based on the aggregate of those fees).

I see this as a huge opportunity for the banks similar to what we’ve witnessed with HVCC. This is their big chance to control where escrow and title go–to them! Banks will state that they do not want to risk being off on their quotes with new binding good faith estimates and it’s my belief they will do their best to keep escrow and/or title “in house” or affiliated providers. Some mortgage brokers may find that they will have to use the banks preferred title and escrow vendors just as they do the banks appraisal management companies. Should this happen, we may see banks use low cost centralized services, similar to many bank processing centers (some are even located out of state).

How will borrowers know how to select or shop for a title and/or escrow company? Can they rely on their bank loan originator to help them select a title or escrow provider when the MLO (Mortgage Loan Originator) is directed to only have the bank’s providers on the list? The new RESPA laws will not allow MLOs to recommend anyone who is not on the service provider list. Should the consumer rely on their real estate agent to recommend the title and escrow provider (many brokerages have joint venture relationships)?

With a purchase, if the title and/or escrow service providers are other than those designated on the written service provider list, then it is presumed that the buyer/borrower selected those providers (even if it was directed by the real estate agents or seller) since the buyer agreed to the contract. With this scenario, the lender is not subject to the 10% tolerance in fees for those costs. Buyers may find a surprise comparing the good faith estimate at signing to the HUD Settlement Statment if the title and/or escrow company are different from what was designated on the purchase and sales agreement.

The new Good Faith Estimate may wind up being a huge set back for independent escrow companies and smaller independent title agencies who will most likely lose any relationships they have forged with loan originators who happen to work for one of the big banks.

By the way, if you are planning on selecting your escrow and/or title provider. You may want to start researching prior to your prequalification process with the mortgage originator. You may find that effective January 1, 2010 most mortgage originators will not want to provide a good faith estimate until you have committed to working with them as the new GFE’s are binding for the loan originator unless certain “changed circumstances” permit the MLO to issue a revised estimate. Per HUD:

“If a GFE is given during prequalification, the receipt of one of the six required pieces of documentation will not constitute a “changed circumstance.”

The loan originator is presumed by HUD to have the “six required pieces of documentation” if they issue a good faith estimate.

…I’ll be writing more about this on a future post.

Ardell posed a question on her last post about credit scoring that I’ve been meaning to address here at Rain City Guide on how credit scores are impacted by short sales or foreclosure. When I was speaking at the Mortgage Girlfriends Mastermind Retreat in Scottsdale this summer, I had the opportunity to meet Linda Ferrari, a well known credit expert and author of “The Big Score – Getting It and Keeping It” (a book I highly recommend everyone read).

According to Linda, “a foreclosure can drop a credit score 50-250 points (this includes points all ready lost to delinquent payments). The difference in point loss depends on how many points someone has to lose in the payment history factor of his or her credit report. Thus is someone has a 750 credit score and they opt to foreclose, their score could drop 250 points. However if someone has a 500 credit score, they may only lose 50 points for the same derogatory.”

It hardly seems fair to me that someone who has established excellent credit and they are faced with a huge financial hardship, they’re penalized on a greater scale simply because they have “more to lose” (reminds me of our income tax system)! With a foreclosure, you can expect to wait about 5-7 years to purchase your next home (based on current guidelines) assuming a mid-credit score of 680 and a 10% down payment for conventional financing.

A deed in lieu of foreclosure may impact credit scores the same as a foreclosure depending on how it is reported to the credit bureaus–they don’t have to report it as a foreclosure…if they do, the credit will be scored as such. Here’s what Linda recommends you try negotiating how the deed in lieu is reported on your credit with the lender in preferred order:

Paid As Agreed. Credit scores will have already dropped over 100 points due to default in payments; however, if reported as Paid As Agreed, the borrower will be able to purchase another home in a shorter time period. Paid Settlement. Credit scores could drop 75-100 points in addition to the points already lost for delinquent payments. Foreclosure. Credit scores could drop 100-150 points in addition to the points already lost for delinquent payments.

One advantage of a deed in lieu of foreclsoure is you may be able to purchase a home, if you so desire, a minimum four years afterwards with 10% down payment, based on current guidelines.

A short sale is potentially the least damaging to your credit scores assuming you’ve been able to make mortgage payments on time. According to Linda, credit scores may drop from 50-150 points (depending on what else is going on with your mortgage and credit history). You may also be able to buy a home quicker using this route. Linda Ferrari writes on her blog why you may not want to consider using a short sale as an option should you be in financial distress.

FHA may allow borrowers who have lost a home due to short sale, deed in lieu or foreclosure a little quicker than conventional financing–around three years depending on various factors. Extreme extenuating circumstances may allow for a shorter time period. Again, this is current guidelines. I wouldn’t be one bit surprised to see FHA change this guideline to be more in line with conventional financing.

You have to keep in mind that credit scoring is accumulative, everything is factored to come up with those three scores that are suppose to reflect your current credit. The only real good news about credit scoring is that your scores are temporary–they are changing constantly. Pay down a credit card, establish good payment history on your installment loan and your scores will improve over time.

There are few things more important to me than a home buyer being able to qualify themselves, vs. taking anyone else’s word for the answer to “How Much Home Can You Afford?” Since I am a real estate agent and not a mortgage professional, I like to post a laymen’s view at least a couple of times a year on this topic. This simplistic approach should be any potential homebuyer’s first step in “the process”. I also think that any Buyer’s Agent should go through this detail with their clients before assisting them in making an offer on a house, so consider this an agent tutorial post as well.

There are many easy to use Mortgage Calculators like this one on Zillow. But just as you should know that 6 times 3 is 18 without needing to use a calculator, you should know WHY the online mortgage calculator is spitting out a number. If you know that 6 times 3 is 18, you will know if the calculator sums that out at 37, that you or it did something wrong. Same with Mortgage Calculators and Pre-Approval letters. You should know enough to know when the answer is outside of most people’s “comfort zone”.

Back to the online mortgage calculator. The first data field you need to fill out is “current combined annual income“. You need to know a few things to answer that question correctly.

1) When they say “income” they mean GROSS income, not your take-home pay.

2) If you are salaried, and make the exact same amount every paycheck, then your current salary is what goes in that data field. If any portion of your income is based on an hourly rate or a bonus for production, then your most recent income information is not usable. Unless it is a promise to pay (salary), then your “annual income” is determined by averaging your last two years worth of income AND is subject to subjective changes by the lender’s underwriter. Sometimes that happens a week before closing! So best to qualify yourself using projected, realistic potential outcomes.

If you just got a raise from $75,000 a year to $85,000 a year, and none of that $85,000 is subject to change based on hours worked or bonus income, then the full $85,000 a year goes in that box.

If you made $85,000 a year of which $60,000 is salary and $25,000 is overtime and/or bonus income, then $85,000 is NOT what you put in that box. If you had overtime and bonuses of $15,000 last year and $25,000 this year, then you add the two together and divide by 2, making your annual gross income $60,000 salary plus $20,000 of overtime and bonus pay. HOWEVER, if it is the reverse and you had $25,000 last year and $15,000 this year…not likely the lender is going to look at a figure higher than $15,000. They may impose a continued downward trend on that recent $15,000 earning vs. $25,000 the year before. In fact they could exclude it altogether as an unreliable source of income, unless your employer produces a letter guaranteeing that the overtime and bonus income will not drop below $15,000 for the next year or two.

3) “monthly child support payments” is the next line in that particular “mortgage calculator” and is the only additional income category. That doesn’t seem right at all to me. Best to contact a lender regarding all of your “other income” sources to determine which, if any, they will use. What if your child support payments are ending in 8 months? What about interest income, alimony payments, etc.? Unless you need to use these other income sources to qualify, and expect them to continue for the life of the loan, or at least for 10 years, I would suggest not including this “other” income. It will give you a “cushion” of extra monies if needed. Buy a home you can afford without these extra income considerations, if at all possible. More on this when we get to “back end ratio”.

Back to the handy but not so accurate online mortgage calculator it makes no sense to me why they would ask for HOA dues in the “income-debt” portion and then again when getting to estimated monthly payment for the new loan. In fact the whole “income and monthly debt obligations” section is poorly worded for accuracy. Once you get past income, you want to calculate your monthly “debt” payments. The most common of these are”

Car payments, Student loan payments, credit card payments, alimony or child support payments (though technically not “debt”). What you do not include are regular living expenses like utilities, gas, car insurance…all of these are not “debt’ payments.

Now skip all the way to the bottom and see the terms “front end” and “back end”. The calculator has a pre-set for 28% front end and a 36% back end. it allows you to change these pre-sets, but do not do that until you understand the numbers using the pre-sets. Assume that the pre-sets are the Average Comfort Zone for most people.

“Front-end” is your housing payment. “Back-End” is your total debt PLUS your housing payment. Old school rules work like this:

You make $10,000 a month gross at 28% = $2,800 a month for housing payment “front-end”

You make $10,000 a month gross at 36% = $3,600 a month for housing plus debt payment “back-end”.

IF your debt payments are $1,000 vs the $800 allowed, then your front end should be $2,600 vs. $2,800. $3,600 back end minus $1,000 = $2,600, so your “back end being out” reduces the amount available for housing payment by $200.

BUT that does not work in reverse. If you have NO DEBT, your housing payment stays at $2,800 and DOES NOT increase to $3,600. This based on how likely is it that you will have no debt for 30 years?

That last paragraph is the most important paragraph in this post, so take the time to understand it well.

28% front end and 36% back end has been the long term conservative approach since forever. It is also very rare that a lender will use these ratios when qualifying you for a mortgage, so YOU must do it yourself. Then when you know your payment should be $2,600 and the lender qualifies you for a payment of $3,500, you know just how much your lender is stretching you outside of conservative standards. That tells you how difficult it may be for you to actually make that payment for the next 3-5 years. A family with 4 children might only be able to spend 20% to 25% of their gross income on housing payment. A single person with a high income may be able to stretch to 33% of their gross income on housing payment. If you are a VA buyer…this is very important, as VA uses one ratio and not two (last I looked) allowing you to spend your full back end allowance on housing payment if you have no current debt.

One of the things that prompted me to write this post today was this comment I saw from a lender on Zillow:

The rules are still tightening-to a fault. Fannie Mae will soon be announcing that they are going to a 45% back end ratio and any borrower with a 620 fico score has to put down at least 20 percent. I can live with the 20 percent for a 620 fico,but the 45% back end ratio is going to make it even more difficult…

As you can see, lenders are not used to people qualifying at a conservative standard of a 36% “back end ratio” and are complaining that the rules are too tight when requiring a 45% back end ratio. OUTRAGEOUS! Remember we are using GROSS income and not net income. So 45% of your gross income on housing payment and debt is clearly NOT too “tight” of a rule.

Knowing how to qualify yourself using 28% front end and 36% back end, will help you know for yourself what monthly payment you truly can afford. Here’s my suggestion: If conservative ratios say you can afford $2,800 for a housing payment, and your lender says that number should be $3,500, test it first. If your current rent payment is $1,700, try putting $3,500 minus $1,700 in the bank every month (not on average). If you can’t put an additional $1,700 a month in the bank easily, each and every month for at least 6-9 months, don’t consider buying a house at the max your lender “says” you can afford.

In fact regardless of the ratios, it’s a very good idea for you to pretend you have that new housing payment well in advance of making an offer to purchase. Test for yourself, by banking the difference, before taking on that 30 year obligation to pay.

The Seattle Times reports that Seattle is returning to a neighborhood-based system. Given it has been about 30 years since Seattle abandoned that system, this is big news for everyone who lives in Seattle, particularly people who are buying homes in Seattle.

According to the article, this decision passed by unanimous vote last night at 11 p.m.

If we’re going to use our limited resources efficiently, this is a big opportunity to reduce transportation costs, balance out enrollment so that hopefully the vast majority of our schools have enough students in them to be successful,” said board president Michael DeBell.

When people are looking for homes to buy, having a geographically based school system is very important. Not knowing which school your child is likely to attend adds a layer of uncertainty to an already uncertain process. I’m sure this decision will be controversial, but I have to agree that when an entire community is vested in the success of the “neighborhood” school…the system will improve via more outside support. Also, it will be easier to target the schools and communities that need more support than the local community can itself provide.

I went to the school around the corner from my house. I could even see inside the school from my yard. My children always attended the school nearest my home, and I used “which school?” as the basis for my home buying decision. Parents and children from the neighborhood around the school volunteered to help with seasonal maintenance projects and had a vested interest in the school being a safe and attractive neighborhood component.

On all counts, I think this is a good decision. Still I expect it will have as many unhappy constituents as it has happy supporters, until the system is in place long enough for people to forget the three decade old “used to be”.

In a press release this morning, Fannie Mae announced a new program for homeowners who are facing foreclosure and who do not qualify for a loan modification: Deed for Lease. Distressed homeowners would complete a deed in lieu of foreclosure back to the lender anad then rent their home from the lender at market rate. Leases may be up to 12 months followed with a month to month option.

Jay Ryan, Vice President of Fannie Mae says:

“This new program helps eliminate some of the uncertainty of foreclosure, keeps families and tenants in their homes during a transitional period, and helps to stabilize neighborhoods and communities.”

For homeowners to qualify for the Deed for Lease Program:

I’m wondering if this will be considered a taxable sale — will there be excise tax due? A title insurance policy will be required to prove the title is “marketable”. The properties will be inspected to make sure the occupants have kept the home in good condition and to permit the marketing of the property for sale. I would hope that the Deed for Lease tennant would have the first right to re-purchase their home during the 12 month period. According to Fannie Mae’s announcement:

“A Deed for Lease property that is subsequently sold includes an assignment of the lease to the buyer.”

Homeowners will need to work directly with their mortgage servicer (who they make their mortgage payment to) in order to see if they qualify. According to Fannie Mae, mortgage servicers can offer this program immediately–however, you can bet it may take a while for this program to become available. Fannie Mae offers these instructions for homeowners who are considering this program.

I’m wondering if there is excise tax due on the sale of the property to the lender.

The intent of the program, which I applaud, is:

“to minimize family displacement, deterioration of neighborhoods caused by vandalism and theft to vacant homes, and the effect these have on families, communities and home price stabilization”.

I’m sure we all have abanoned homes in our neighborhoods and know families who have lost their homes. Hopefully this will help make things a little better for all while our housing industry and our economy is trying to recover.

Post Updated based on Info available as of 11/5/09 – No significant changes, but a few minor ones, so if you first read this back when I wrote it on 10/29/2009, take another look at the updates.

There are a lot of rumors flying around suggesting that the $8,000 credit has been extended. While that is not the case, as nothing has been signed yet, there seems to be strong support for:

There are a lot of rumors flying around suggesting that the $8,000 credit has been extended. While that is not the case, as nothing has been signed yet, there seems to be strong support for:

1) Extending the $8,000 credit for 1st time buyers, including people who have not owned a home for 3 years

2) An added $6,500 credit for move up buyers who have owned their current home for at least 5 consecutive years of the last 8 years. (this provision is still under heated discussion and most subject to compromise before the bill is passed.) Updated 11/5/08

3) Expansion of the income requirement to $125,000 for an individual and $250,000 $225,000 for a married couple.

4) Extension to contracts entered into by April 30, 2010 that are also closed by June 30, 2010 (before July 1, 2010)

The most credible “rumor”/story going around [IMO] is CNN Money’s “$8,000 Credit Still in Play“.

In my opinion #1 and #4 make the most sense in that it seems senseless to drop the credit at the end of “Spring Bump” vs. just before 2010 “Spring Bump”. Closing the door on the credit on Nov. 30th never made any sense, as seasonal factors will make it appear that the credit going away is having more of an adverse affect than it really is, given November through February sales are almost always lower as to price and volume.

Cutting the cord on the credit at the end of April (end of March even better) makes perfect sense, and gives the market the opportunity to compensate during its most robust season. If the market can transition from 1st quarter 2010 with a credit, to 2nd and 3rd quarters without a credit on a flat market basis, it will be easier to get rid of it altogether. And yes…eventually…it really must go away. I certainly hope the industry isn’t going to keep lobbying indefinitely for its continuation. That would NOT be a good thing.

While it seems that “Senator’s Have Agreed” this credit is still not signed sealed and delivered, (Update 11/5/09 at last step, needs to be signed by the President) so stay tuned for the final version as I think the wheel may still be spinning with regard to the $6,500 move up buyer credit, as well as the expansion of the income requirements.

This home is in Snohomish and is probably familiar to a few who visit the area or live in the community.

Homes that seem made for Halloween

Today, during the Washington Association of Mortgage Professional’s State “Connect” Convention, Raincityguide author Rhonda Porter was presented with the Jim Fitzgerald Distinguished Service Award for her outstanding contribution to the mortgage broker and lender community. Presenting the award was Rhonda’s brother-in-law John Porter who received the same award from his father, Bob Porter, who ALSO received the award. Yes, mortgage lending does have a way of running in the family.

Jim Fitzgerald passed away in April of 1999 at the young age of 48. He was President of the Washington Association of Mortgage Brokers in 1994 and an active member of WAMB,* working tirelessly on behalf of the membership. “Jim worked hard to bring the Association up to a new level.” John Porter said, “People knew Jim all over the country even before social networking started. This is the most honorable award I ever received and I am so proud to present this to my sister-in-law.”

This year Rhonda volunteered to be the WAMP Social Media Chairman. She created a facebook page for the Association and helped organize two Social Media RE Bar camps during these last few months and has volunteered her time to help mortgage professionals here in Washington State and in other states learn how to effectively and professionally participate in social media.

Rhonda, we are all proud to know you.

*WAMB is now WAMP

Wash Assoc of Mortgage Brokers changed their name in 2008 to the Wash Association of Mortgage Professionals

Below, WAMP President Jason Bloom with Rhonda Porter.